With real estate being so competitive, may investors are

investigating real estate mortgages.

This short video explains the variables.. WATCH HERE

Real Estate Note Buyers and Seller Carry Consultants

With real estate being so competitive, may investors are

investigating real estate mortgages.

This short video explains the variables.. WATCH HERE

It is not unusual for a note holed to sell their note to get a certain amount of cash. But………….when given a quote by a note buyer many time they are shocked at the huge discount and insulted—maybe even angry that a note broker or buyer would try to “steal” their “good” paying note. Any proficient note buyer / broker will offer alternatives in the form of quoting to buy a piece or just some of the outstanding balance. Have you ever bought a full pizza? Have you ever bought just a few pieces of piz za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

Sometimes as a note owner you only need a specific amount of cash. Selling the whole note makes no cents. There are multiple ways to architect a partial sale. You can sell 12, 24, 60,100 or however many of payments to bring you the cash your need. For the next x# of months, those payments would go to the partial note buyer. After the buyer is paid back, the remaining payments would revert back to you.

Selling a partial gives the note seller a great amount of flexibility. Partials are always a great tool to use when the note holder has an immediate cash requirement and only needs a specific amount of money to cover a specific situation or for a specific purpose. A partial minimizes the discount and frees up cash. It is the best of the best. The terms of the note remain the same for the note payor/borrower. The only thing that changes is the payments are directed to the third party servicing company. Additionally there is contractual language giving the partial buyer the right of first refusal to buy additional payments if they so choose.

What about an early payoff?

Many notes do pay off early. The average time a house or note is paid off historically is 7 – 10 years. If it is paid off early, there are contractual agreements / documents from the outset that are managed by the third party note servicing company determining the payoff and or re-conveyance.

What if the note goes into default?

Unfortunately some notes/mortgages do go into default. IT is a realty of the financial world. If in fact that happens, the contractual agreement spells out the options. Either a buy back from the partial buyer or proceed with the foreclosure /eviction process with the goal of taking back the property and resell it for fair market value. Both the original note buyer and the partial buyer benefit. The partial buyer is made whole with the balance going to the original note seller.

Three Real Life Case Studies

Houston, TX 11/30/15 – Single Family house

Gerry owned a note on a single family house in a so-so area of Houston. He needed money for some personal issues and needed help. I offered to buy the full at a larger discount due to the issues noted below. He was not real enthused with the offer, so we agreed to a partial purchase.

Deal Points

Good Points

Gerry negotiated a great terms with a sort-of strong buyer. Meaning the buyer put down a very strong $14,000 on a $60,000 purchase resulting in a great Loan to Value(LTV). The 7% interest rate was OK. It had a relatively short amortization period of 60 months with a great on time pay history. The 3 Buyer’s FICO scores were weak, but they had a good job history.

Marginal Points

Due to the drop in oil, Houston lost 44,000 jobs. The neighborhood had some marginal houses, but in the process of changing for the good. For these two items, if felt uncomfortable with a full purchase.

Bottom Line

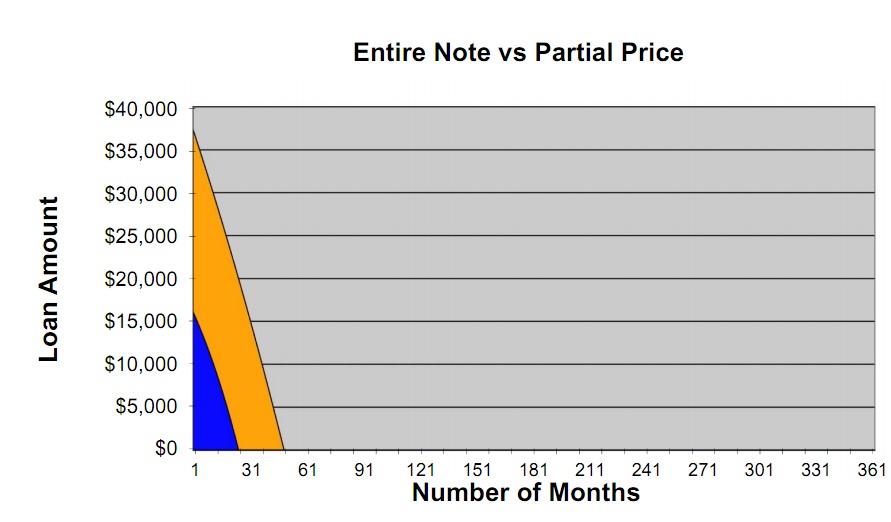

We bought a 24 month partial with the option to purchase the balance in 15 months. It was a secure, safe purchase and Gerry received what he needed. Out Investment to Value was a very secure 26% with a safe Loan to Value of 57%. The graph depicts what we purchased(blue) and what the seller kept. Within one year we bought the gold portion all in our IRA.

Fast forward 11/30/16

Gerry called requesting if Capstone would be interested in purchasing the balance of his note. He had a lingering debt situation. After a short due diligence period, we closed within 10 days. Again Gerry was happy and we were happy owning the full note. Three weeks later we sold the full note to one of our Note Investor Forum Meetup attendees for his ROTH IRA.

Summary

The note seller had a situation, we provided him a solution—twice. The Meetup attendee was in his early 70’s. He wanted a higher yielding note with a shorter amortization period. This was his first note purchase. He is excited to buy additional opportunities.

_____________________________________________________________

Salem, OR 12/20/16 – Land Parcel

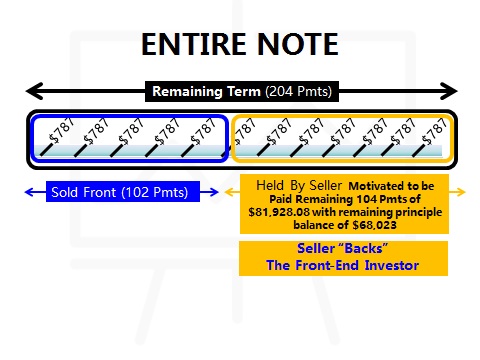

A note colleague referred his friend Kirt his client, Joyce who owned a 13.17  acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

Deal Points

Good Points

Joyce’s buyer had a very good job as a helicopter pilot earning close to $150,000/yr. The servicing company provided a very stable 36 month payment history. She also had a survey of the land which had all utilities. Most likely in the future the apartment complex would expand—buying out the pilot and our partial.

Marginal Points

Joyce did not negotiate good note terms. Only a 4% interest rate (her realtor said that was fair). In reality for land it should have been at least 10%.

Bottom Line

We bought a 102 month partial with the option to purchase the balance in the future. It was a secure, safe purchase and Joyce received the funds she needed. We had a very strong ITV of 11% . It was a true win-win. Our referral partner received a referral fee and sold some gold to Joyce. Joyce was able to buy her house and the Capstone investor had a very safe and secure partial note investment in her mothers’ IRA.

Fast forward 4/5/17

Joyce called stating that she wanted to sell the remaining 102 payments ($68,023) which we did for $19,377. She did not want to wait 102 months to cash out the remaining payments. Joyce got what she needed and we received a fair deal. On the entire transaction, our Investment To Value (ITV) was a very safe 17%, in a fast appreciating real estate market. The odds are high the parcel will be sold for development in the near future providing the investor a very nice return because she bought the note at a steep, but fair discount due to the 4% note rate.

Summary

What really happened though is even more normal. Joyce calls back wanting sell the rest of the back-side far before the re-assignment period. Many not sellers buy into a partial transaction because the transaction mitigates the discount. But…………..more often than not, they will want to sell the remaining balance early to meet life needs.

Partials are a unique method of meeting many needs for note buyers and sellers. They should not be over looked. It is an incredible passive investment vehicle for your ROTH IRA

This Case study was/will be presented at the Note Investors Summit April 5-7, 2018 in Irvine, CA

Hedge fund manager and former Goldman Sachs partner Steven Mnuchin  confirmed to CNBC on Wednesday morning that President-elect Donald Trump has nominated him for the position of Secretary of the U.S. Department of the Treasury.

confirmed to CNBC on Wednesday morning that President-elect Donald Trump has nominated him for the position of Secretary of the U.S. Department of the Treasury.

Trump’s choice of Mnuchin, 53, who served as the President-elect’s national finance chairman during his campaign, is considered controversial because Mnuchin has never worked in government and his roots in Wall Street would seem to conflict with Trump’s anti-financial industry sentiment during his campaign.

One area where he does agree with Trump, however, is the need for reduced regulation. Mnuchin laid out a number of his initiatives on CNBC’s Squawk Box, should the U.S. Senate confirm him as the 77th Treasury Secretary. One of those is to roll back the Dodd-Frank Wall Street Reform and Consumer Protection Act, which passed in 2010 and is considered by the Obama Administration to be one of its greatest achievements. In various speeches and interviews throughout his campaign and since his election, Trump has vowed to overhaul the controversial financial reform law.

“We (Mnuchin and Trump’s choice for head of the U.S. Department of Commerce, Wilbur Ross, also announced on Wednesday) have been in the business of regional banking, and we understand what it is to make loans,” Mnuchin told CNBC. “That’s the engine of growth to small- and medium-sized businesses. The number one problem with Dodd-Frank is it’s way too complicated and it cuts back lending. So we want to strip back parts of Dodd-Frank that prevent banks from lending, and that’ll be the number one priority on the regulatory side.”

Mnuchin told CNBC that the U.S. economy can sustain a growth level of between 3 and 4 percent. In fact, he called sustained economic growth “our most important priority.”

“It is absolutely critical for the country,” Mnuchin said. “We absolutely can have sustained growth at that level. To get there, our number one priority is tax reform. This will be the largest tax change since Reagan. We’ve talked about this during the campaign. Wilbur and I have worked very closely together on the campaign. We’re going to cut corporate taxes, which will bring huge amounts of jobs back to the United States. We’re going to get to 15 percent, and we’re going to bring a lot of cash back into the U.S.”

In an interview with Fox Business after the announcement of his nomination, Mnuchin said he believes that the controversial government conservatorship of Fannie Mae and Freddie Mac should end and that the private market should have more of a share in the mortgage market.

“We will make sure that when they are restructured, they are absolutely safe and don’t get taken over again. But we’ve got to get them out of government control,” Mnuchin said, according to Bloomberg.

“A resolution of the conservatorship of Fannie and Freddie appears likely with Mnuchin as Treasury secretary,” says Tim Rood, Chairman of The Collingwood Group. “His experiences at Dune Capital, particularly the IndyMac/OneWest purchase and turn around, will most certainly influence his decision-making calculus.”

Five Star Institute President and CEO Ed Delgado said of the nomination of Mnuchin for Treasury Secretary: “I anticipate that with this new appointment, Treasury will continue to promote the department’s mission by encouraging a strong economy and creating economic growth and stability. As the economy further recovers from the Great Recession it is imperative that the housing industry and Treasury work in hand and hand to ensure housing and economic prosperity.”

Mnuchin left Goldman Sachs in 2002 after 17 years with the global investment banking firm to become vice chairman of hedge fund ESL, and he later became CEO of another hedge fund, SFM Capital Management. In 2009, Mnuchin and a group of investors purchased the failed Pasadena-based IndyMac bank from the FDIC for $1.5 billion after the mortgage meltdown and renamed the bank OneWest. In the years immediately following the crisis, OneWest’s foreclosure practices generated considerable controversy, particularly in California.

Mnuchin’s hedge fund, Dune Capital Management, of which he currently serves as CEO, became involved in Hollywood motion pictures years ago, financing such box office hits as “X-Men” and “Avatar.”

“If he gets the post, Mnuchin will bring a lot of mortgage expertise to the Treasury Department,” says Rick Roque, President of Menlo. “He bought Indymac, renamed it OneWest and then sold that company to CIT Group in 2015. That kind of experience, in addition to his experience in sub-prime origination, retail origination, and correspondent channels will prove to be very valuable to the non-depository mortgage banking market.”

Accepting payments on the sale of real estate might have made sense at the time, but circumstances change.

Accepting payments on the sale of real estate might have made sense at the time, but circumstances change.

Many sellers discover they would now prefer cash today rather than the small amount that trickles in each month.

Here are just a few reasons people have sold all or part of their seller financed mortgage notes for cash: