![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

Real Estate Note Buyers and Seller Carry Consultants

![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

S&P/Case-Shiller released the monthly Home Price Indices for March (“March” is a 3 month average of January, February and March prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: S&P CoreLogic Case-Shiller Index Shows Annual Home Price Gains Continue to Weaken

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.7% annual gain in March, down from 3.9% in the previous month. The 10-City Composite annual increase came in at 2.3%, down from 2.5% in the previous month. The 20-City Composite posted a 2.7% year-over-year gain, down from 3.0% in the previous month.

Las Vegas, Phoenix and Tampa reported the highest year-over-year gains among the 20 cities. In March, Las Vegas led the way with an 8.2% year-over-year price increase, followed by Phoenix with a 6.1% increase, and Tampa with a 5.3% increase. Four of the 20 cities reported greater price increases in the year ending March 2019 versus the year ending February 2019.

(NOTE: The Phoenix Market did a complete u-turn NORTH. 45% of all inventory was sold in April. What was a down turn, is now back on track. The Phoenix area is growing by 86,000 people every year. Maricopa County is the fasted growing county in country. CLICK HERE FOR THE LOCAL REIA STATS

Property Locations

IL IN MI OH TN

BPO Range: $33,000 – $70,000

UPB RANGE: $17,785 – $34,860

PURCHASE PRICE RANGE: $19,000 – $26,200

PRICING RANGE: 76% to 90% of UPB

Re-Performing Loans & Seasoned Performing Loans

Click Here to Access

CASE STUDY 3

This post is a 3rd in a series of 4 regarding how a perfectly good performing note goes south due to life event situation.

This particular note was in the small town of Marshall, IN. The note -Contract for Deed- was originated in 2009. The payors significant other passed in 2010. My IRA purchased the note in 2015. The note was scheduled to mature in June, 2019. I was unaware of the loss of the male payor. The payment history evolved into a rolling 120 days, meaning after 4 months the payor paid the balance or part of the balance to stay out of the forfeiture procedure. However this payment history caught up with the payor in that there was a $5,000 unpaid balance balloon that went beyond the due date of the note.

Fast forward to February, 2019, I was tired of constantly contacting the payor. I did not want to go thru the forfeiture process as to take back the house –due to condition, was not a viable option. Plus 9 months and $3,000 in attorney fees were not viable. In prior conversations, it was discovered she was the caregiver of her mother and was not working. He current husband was not working. After multiple conversations, she realized she needed help. Her Dad was brought into the conversation. He agreed to help her out. They agreed to bring the payments current. In exchange to removing the deceased payors name from the CFD, they agreed to a loan modification which extended the term 12 months, and stay current. If they ran late past 15 days, the newly executed Quit Claim deed would be recorded and my IRA would own the house.

It was a win-win. The payor benefited by having the deceased partner removed from any claim of ownership, the loan was brought current, I avoided the possibility of a 9 month forefeiture procedure and the payor will own her house free and clear in 12 months with the extension of the balloon due date.

Even though the remaining balance was small, the solution was perfect for all.

I have learned, if one works with the payor and developes a dialog, future unfortunate events can be worked out much easier. But, it is all about how can the payor feels and appreciates that they are being helped so they will be open to a solution which also benefits the note holder in the event needed.

This case study was presented at the May 1 Note Investors Forum Meetup

As discussed in my prior blog, Note workouts are not rocket science. It is a matter of treating every party fairly.

CASE STUDY 2

This 2nd case study happened on a 2nd Mishawaka, IN property. My

partner & I bought a non-performing note(NPN) in October, 2014. The payor had become functionally unable to do anything due to a debilitating disease and had been out of the house for 2 years. We tried a workout which was not viable but did get a deed in lieu of foreclosure with cash for keys.

After fixing the place up, we found a recently divorced lady. She was happy with a probtionary rent-to-own for 12 months a and Seller-carry to follow with 10% down. She was also qualified by an RMLO oer Dodd-Frank. We sold the 1st note to a partial note investor and kept the second.

Fast forward, the payor stopped paying due to illness. Again we developed a good working relationship with her. After a series of discussions, she confirmed that she really did want to stay and agreed to a loan modification. The “we” was the partial note buyer.

The end result is after consulting with our legal counsel and her daughter, the payor signed a Quit Claim deed to be held in escrow and agreed to a payoff schedule for her to get caught up on the back payments. If she falls behind on any payment for more than 15 days we can record the Quit Claim deed. My company will own the house. We have avoided the the foreclosure process to boot. The bottom line: the payor is happy and agreed to bring the loan current, the partial buyer is happy as she is geting paid, my partner is happy as we are both collecting on our second and have avoided a negative situation –the long forfeiture process.. This was/is a total win-win.

Potentially, we may have to record the deed and rehab, but for now it is all good.

I have been in the note space in various ways since 1985 with the purchase

of 20 acres in Scarborough, ME which was developed into 17 house lots. The last lot I sold with seller-carry.

To that point, in the last 14 months 4 notes have taken a turn for the worst and required developing a work out strategy to protect my interests or if a partial to protect the interests of the partial buyer.

Currently I buy, keep, create partials and broker notes from around the country. Mostly performing notes | Contract for Deeds. Very rarely do I purchase non-performing notes. It just is not my thing. However, notes can and do go bad. The payor has personal issues, etc. Life just happens.

CASE STUDY 1

I purchased a performing note in Mishawaka, IN in 2015. Great #’s great pay history. Good colateral. I found a buyer to fund the purchase via selling a partial and in effect a double close. It was good for them and good for my ROTH. Fast forward to April, 2018, the payors health took a turn for the worst. They called the servicer stating they would not continue paying and were going into a Bankruptcy. My 1st challenge was to keep my partial investor whole. I made up 4 months to the partial buyer, completed a deed in lieu with the payor, rehabbed the house and resold it in February, 2019 at which time the partial buyer was made whole. Throught the process, the partial buyer was in the loop and concurred with the workout and dispostion. They were made whole at the COE. A couple of months later they thanked me stating it was all good especially the net 11% return. To boot my ROTH cleared $20k on a small value asset of < than $70,000. It was a win for everyone. Even on a lower value property.

Note workouts are not rocket science. It is a matter of treating every party fairly.

The November 7th Note Investors Forum will be hosting –Howard Tenn

of Asian Night Capital. This will be an enlightening presentation on

How to Pitch a to a Private Investor. Click on picture for 68 second overview

Tickets can be purchased at

The following article appeared in DSNEWS.

House prices are rising.

There is a shortage of housing.

There is a shortage of rentals.

There is a shortage of well priced notes & REO’s.

“Prices are growing more quickly in some places than in others, and in MSAs where recovery has been most robust (and even in surrounding metros), price growth is probably not the best metric to use for rental investors seeking a new property to buy and hold.

So………….which MSAs have the best rate of return on rental investments?

The following article was from CNBC.

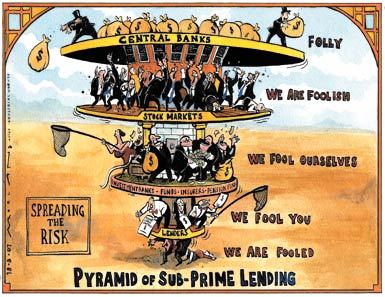

Having lived and felt the pain of the subprime crisis, the return to subprime is a recipe for disaster. No different than the movie The Big Short or the book Fools Gold!!

They were blamed for the biggest financial disaster in a century. Subprime mortgages – home loans to borrowers with sketchy credit who put little to no skin in the game. Following the epic housing crash, they disappeared, due to strong, new regulation, and zero demand from investors who were badly burned. Barely a decade later, they’re coming back with a new name — nonprime — and, so far, some new standards.

California-based Carrington Mortgage Services, a midsized lender, just announced an expansion into the space, offering loans to borrowers, “with less-than-perfect credit.” Carrington will originate and service the loans, but it will also securitize them for sale to investors.

“We believe there is actually a market today in the secondary market for people who want to buy nonprime loans that have been properly underwritten,” said Rick Sharga, executive vice president of Carrington Mortgage Holdings. “We’re not going back to the bad old days of ninja lending, when people with no jobs, no income, and no assets were getting loans.”

Sharga said Carrington will manually underwrite each loan, assessing the individual risks. But it will allow its borrowers to have FICO credit scores as low as 500. The current average for agency-backed mortgages is in the mid-700s. Borrowers can take out loans of up to $1.5 million on single-family homes, townhomes and condominiums. They can also do cash-out refinances, where borrowers tap extra equity in their homes, up to $500,000. Recent credit events, like a foreclosure, bankruptcy or a history of late payments are acceptable.

All loans, however, will not be the same for all borrowers. If a borrower is higher risk, a higher down payment will be required, and the interest rate will likely be higher.

“What we’re talking about is underwriting that goes back to common sense sort of practices. If you have risk, you offset risk somewhere else,” added Sharga, while touting, “We probably are going to have the widest range of products for people with challenging credit in the marketplace.”

Carrington is not alone in the space. Angel Oak began offering and securitizing nonprime mortgages two years ago and has done six nonprime securitizations so far. It recently finalized its biggest securitization yet — $329 million, comprising 905 mortgages with an average amount of about $363,000. Just more than 80 percent of the loans are nonprime.

Investors in Angel Oak’s nonprime securitizations are, “a who’s who of Wall Street,” according to company representatives, citing hedge funds and insurance companies. Angel Oak’s securitizations now total $1.3 billion in mortgage debt.

Angel Oak, along with Caliber Home Loans, have been the main players in the space, securitizing relatively few loans. That is clearly about to change in a big way, as demand is rising.

As a real estate note professional, the buyer of performing and non-performing notes & REO, the following article confirms/addresses what has been shared from many venues.

The nation has a staggering shortage of 7.2 million affordable and available rental homes for extremely low-income (ELI) renter households, reports MFE sister brand Affordable Housing Finance. Deputy editor Donna Kimura examines a new study from the National Low Income Housing Coalition (NLIHC), The Gap: A Shortage of Affordable Homes, which finds that for every 100 of the lowest-income renters, or those earning 30% of their area median income, there are just 35 homes affordable and available to them.

“This leaves over 8 million of the lowest-income people [spending] more than half of their limited income on rent each month, leaving very little for healthy food, for savings, or to cover an unexpected financial emergency,” says Diane Yentel, NLIHC president and CEO. “The report highlights the urgent need for an increased national investment in more homes affordable to the lowest-income people.”

Yental also noted that federal housing programs serve about 5 million low-income households, but the needs of many more families go unmet. Only one out of every four eligible families receives the help they need. As a result of the housing shortage, low-income unassisted households are often severely cost burdened and pay more than half of their limited income on rent.

The severe shortage of rental homes affordable and available to the lowest-income households predates the Great Recession but has worsened in recent years, according to the study. In 2007, 40 affordable and available rental homes existed for every 100 ELI renter households and 67 existed for every 100 renter households with incomes at or below 50% of the area median income (AMI). A small surplus of affordable and available rental homes existed at 80% and 100% of the AMI in 2007. Since then, the supply of affordable and available rental homes (relative to demand) has declined even at these higher-income levels. Renter households at 100% of the AMI, however, still enjoy a surplus nationally and in most markets.