![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

Real Estate Note Buyers and Seller Carry Consultants

![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

I have been in the note space in various ways since 1985 with the purchase

of 20 acres in Scarborough, ME which was developed into 17 house lots. The last lot I sold with seller-carry.

To that point, in the last 14 months 4 notes have taken a turn for the worst and required developing a work out strategy to protect my interests or if a partial to protect the interests of the partial buyer.

Currently I buy, keep, create partials and broker notes from around the country. Mostly performing notes | Contract for Deeds. Very rarely do I purchase non-performing notes. It just is not my thing. However, notes can and do go bad. The payor has personal issues, etc. Life just happens.

CASE STUDY 1

I purchased a performing note in Mishawaka, IN in 2015. Great #’s great pay history. Good colateral. I found a buyer to fund the purchase via selling a partial and in effect a double close. It was good for them and good for my ROTH. Fast forward to April, 2018, the payors health took a turn for the worst. They called the servicer stating they would not continue paying and were going into a Bankruptcy. My 1st challenge was to keep my partial investor whole. I made up 4 months to the partial buyer, completed a deed in lieu with the payor, rehabbed the house and resold it in February, 2019 at which time the partial buyer was made whole. Throught the process, the partial buyer was in the loop and concurred with the workout and dispostion. They were made whole at the COE. A couple of months later they thanked me stating it was all good especially the net 11% return. To boot my ROTH cleared $20k on a small value asset of < than $70,000. It was a win for everyone. Even on a lower value property.

Note workouts are not rocket science. It is a matter of treating every party fairly.

The following article appeared in DSNEWS.

House prices are rising.

There is a shortage of housing.

There is a shortage of rentals.

There is a shortage of well priced notes & REO’s.

“Prices are growing more quickly in some places than in others, and in MSAs where recovery has been most robust (and even in surrounding metros), price growth is probably not the best metric to use for rental investors seeking a new property to buy and hold.

So………….which MSAs have the best rate of return on rental investments?

The following article was from CNBC.

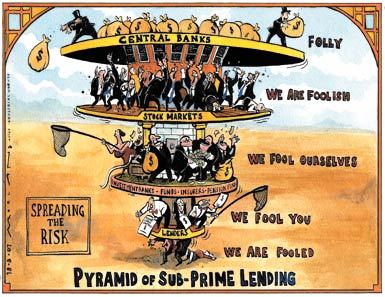

Having lived and felt the pain of the subprime crisis, the return to subprime is a recipe for disaster. No different than the movie The Big Short or the book Fools Gold!!

They were blamed for the biggest financial disaster in a century. Subprime mortgages – home loans to borrowers with sketchy credit who put little to no skin in the game. Following the epic housing crash, they disappeared, due to strong, new regulation, and zero demand from investors who were badly burned. Barely a decade later, they’re coming back with a new name — nonprime — and, so far, some new standards.

California-based Carrington Mortgage Services, a midsized lender, just announced an expansion into the space, offering loans to borrowers, “with less-than-perfect credit.” Carrington will originate and service the loans, but it will also securitize them for sale to investors.

“We believe there is actually a market today in the secondary market for people who want to buy nonprime loans that have been properly underwritten,” said Rick Sharga, executive vice president of Carrington Mortgage Holdings. “We’re not going back to the bad old days of ninja lending, when people with no jobs, no income, and no assets were getting loans.”

Sharga said Carrington will manually underwrite each loan, assessing the individual risks. But it will allow its borrowers to have FICO credit scores as low as 500. The current average for agency-backed mortgages is in the mid-700s. Borrowers can take out loans of up to $1.5 million on single-family homes, townhomes and condominiums. They can also do cash-out refinances, where borrowers tap extra equity in their homes, up to $500,000. Recent credit events, like a foreclosure, bankruptcy or a history of late payments are acceptable.

All loans, however, will not be the same for all borrowers. If a borrower is higher risk, a higher down payment will be required, and the interest rate will likely be higher.

“What we’re talking about is underwriting that goes back to common sense sort of practices. If you have risk, you offset risk somewhere else,” added Sharga, while touting, “We probably are going to have the widest range of products for people with challenging credit in the marketplace.”

Carrington is not alone in the space. Angel Oak began offering and securitizing nonprime mortgages two years ago and has done six nonprime securitizations so far. It recently finalized its biggest securitization yet — $329 million, comprising 905 mortgages with an average amount of about $363,000. Just more than 80 percent of the loans are nonprime.

Investors in Angel Oak’s nonprime securitizations are, “a who’s who of Wall Street,” according to company representatives, citing hedge funds and insurance companies. Angel Oak’s securitizations now total $1.3 billion in mortgage debt.

Angel Oak, along with Caliber Home Loans, have been the main players in the space, securitizing relatively few loans. That is clearly about to change in a big way, as demand is rising.

As a real estate note professional, the buyer of performing and non-performing notes & REO, the following article confirms/addresses what has been shared from many venues.

The nation has a staggering shortage of 7.2 million affordable and available rental homes for extremely low-income (ELI) renter households, reports MFE sister brand Affordable Housing Finance. Deputy editor Donna Kimura examines a new study from the National Low Income Housing Coalition (NLIHC), The Gap: A Shortage of Affordable Homes, which finds that for every 100 of the lowest-income renters, or those earning 30% of their area median income, there are just 35 homes affordable and available to them.

“This leaves over 8 million of the lowest-income people [spending] more than half of their limited income on rent each month, leaving very little for healthy food, for savings, or to cover an unexpected financial emergency,” says Diane Yentel, NLIHC president and CEO. “The report highlights the urgent need for an increased national investment in more homes affordable to the lowest-income people.”

Yental also noted that federal housing programs serve about 5 million low-income households, but the needs of many more families go unmet. Only one out of every four eligible families receives the help they need. As a result of the housing shortage, low-income unassisted households are often severely cost burdened and pay more than half of their limited income on rent.

The severe shortage of rental homes affordable and available to the lowest-income households predates the Great Recession but has worsened in recent years, according to the study. In 2007, 40 affordable and available rental homes existed for every 100 ELI renter households and 67 existed for every 100 renter households with incomes at or below 50% of the area median income (AMI). A small surplus of affordable and available rental homes existed at 80% and 100% of the AMI in 2007. Since then, the supply of affordable and available rental homes (relative to demand) has declined even at these higher-income levels. Renter households at 100% of the AMI, however, still enjoy a surplus nationally and in most markets.

MEETING TOPIC: We’ll walk thru the process of taking a non-performing note to an REO and give examples of how the workout is completed. Basically from purchase to the multiple options to maximize significant returns. We’ll show the passive approach and the more aggressive velocity approach for much higher ROI.

If you have an interest in significantly higher returns than Performing notes, you will want to attend Tuesday April 3rd 11:30am – 1:30pm!!

Look Forward to Seeing You!!!

Dave

RESERVE YOUR SPOT @ EVENTBRITE TICKETS

General Admission / Early Bird Discount price of $16.83

available until Noon April 2nd

Price Includes:

*Admission

*NetWorking

*Education

*Buffet Lunch, Tax & Tip

Just want to show up? No Problem!!

Walkins Always Welcome–$20 @ the door, credit card or cash

includes meal, tax, tip

plus

Networking and Note Training

Email Dave with special dietary needs or special menu needs

Pending home sales rose in December for the third straight month, providing further evidence that 2017 was a positive year for housing, but the National Association of Realtors doesn’t expect the good times to keep rolling.

was a positive year for housing, but the National Association of Realtors doesn’t expect the good times to keep rolling.

Recent data from NAR, the Census Bureau and the Department of Housing and Urban Development showed that 2017 was the best year for new home sales and existing home sales in a decade.

Now, new data from NAR shows that pending home sales rose in December to the highest level since March 2017, but NAR is concerned that Republican-led tax reform will dent home sales in 2018.

According to a new report from NAR, which was released Wednesday, the Pending Home Sales Index, a forward-looking indicator based on contract signings, increased 0.5% to 110.1 in December from an upwardly revised 109.6 in November.

That marks the third straight month that the index has increased.

But combine continually low housing inventory and the Republican tax plan, which President Donald Trump signed into law late last year, and you have a recipe for a slowdown, according to NAR Chief Economist Lawrence Yun.

“Another month of modest increases in contract activity is evidence that the housing market has a small trace of momentum at the start of 2018. Jobs are plentiful, wages are finally climbing and the prospect of higher mortgage rates are perhaps encouraging more aspiring buyers to begin their search now,” Yun said.

“Sadly, these positive indicators may not lead to a stronger sales pace,” Yun added. “Buyers throughout the country continue to be hamstrung by record low supply levels that are pushing up prices – especially at the lower end of the market.”

According to NAR, there’s an “imbalance” of supply and demand, which has led to price increases of 5% or more for each of the last six years, but Yun expects that to slow this year.

Yun said that while tight inventories are still expected to put upward pressure on prices in most areas this year, he expects overall price growth to shrink, with some states even experiencing a decline, due to the negative effect the changes to the mortgage interest deduction and state and local deductions under the new tax law.

“In the short term, the larger paychecks most households will see from the tax cuts may give prospective buyers the ability to save for a larger down payment this year, and the healthy labor economy and job market will continue to boost demand,” Yun said. “However, there’s no doubt the nation’s most expensive markets with high property taxes are going to be adversely impacted by the tax law.”

Three of the states where the tax bill’s changes to property tax deductions are expected to have a significant impact are already threatening to sue the government over the tax bill.

Last week, the governors of New York, New Jersey, and Connecticut said they plan to sue the government due to the Tax Cuts and Jobs Act’s elimination of certain state and local tax deductions.

The tax bill installs a cap of $10,000 on state and local tax deductions, but several states (including New York, New Jersey, and Connecticut) have state and local tax burdens that far exceed $10,000.

Yun said that he anticipates the changes to the SALT deduction rules to disproportionally impact certain segments of the housing market.

“Just how severe is still uncertain, but with homeownership now less incentivized in the tax code, sellers in the upper end of the market may have to adjust their price expectations if they want to trade down or move to less expensive areas,” Yun said. “This could in turn lead to both a decrease in sales and home values.”

Topic

INVESTMENT GOALS & EXPECTATIONS

Our February Note Investors Forum Meeting will followup

on Stan Harley’s presentation– Taking what he shared and incorporating that with with YOUR individual goals. What is most important to you? Cash Flow or Capital Accumulation.

Or……………And more specifically how does risk tolerance fit into your needs and expectations.

We’ll consider Performing and Non-Performing notes

How note due diligence can expand your expectations.

Case studies with 2 special out of state note investors

Click Here for more information

February 6th

Dobson Ranch Inn Fiesta Bar & Grill

1644 S. Dobson Rd

Mesa, AZ

SW Corner of Dobson & RT 60 – Superstition Freeway

Every month Capstone Capital USA, LLC hosts the Phoenix Note Investors Forum. Yesterday January 4, we had the pleasure of having Stan Harley if the Harley Mark![]() et Letter share his Technical Analysis of the Financial Markets. More specifically —TRENDS and CYCLES in REAL ESTATE, INTEREST RATES, and the STOCK MARKET.

et Letter share his Technical Analysis of the Financial Markets. More specifically —TRENDS and CYCLES in REAL ESTATE, INTEREST RATES, and the STOCK MARKET.

There were over 65 luncheon attendees who had the unique opportunity to view the financial  markets from a true market analyst.

markets from a true market analyst.

Bottom line–per Stan, the economy will be fine until 2022 or, then we could be in for some challenging times. The full report can be found here:

Cycles in Home Prices Interest Rates and the Stock Market – Phoenix Area Note Investors  Forum – Stan Harley – January 04 2018

Forum – Stan Harley – January 04 2018

Article originally appeared in CoStar

Most Financial Services Firms Maintain Optimistic Outlook for US Capital Markets in 2018, but Also Advising Note of Caution

Investors and lenders are expected to closely monitor

property fundamentals in the markets and property sectors they invest in for 2018 as the U.S. economy continues its extended recovery now heading into its 10th year.

Despite record low unemployment, increased consumer confidence and a strong stock market, many in the industry see slower growth ahead for rent increases, property prices and overall demand for commercial space. As the capital market moves later into the current real estate cycle, financial services firms are maintaining an optimistic outlook for the U.S. economy, although many are also recommending a cautious approach.

S&P Global Ratings, for example, does not expect a steep correction in real estate prices in the New Year, but is forecasting modest price pressure given slowing fundamentals in light of lower economic growth than in previous years.

There are other risks that could develop, S&P added, that could potentially cause a steeper correction in real estate values, including capital market volatility from a steep equity market correction or sudden spike in interest rates. In addition, bank exposure to CRE is at peak levels and a significant reduction in loan originations could dampen valuations.

In its outlook for 2018, LaSalle Investment Management refers to a Goldilocks environment, in which investors should look for an investment that is neither too ‘hot’ nor too ‘cold’ driven by balanced fundamentals and steady pricing.

LaSalle is expecting debt for real estate to remain plentiful in 2018. At the same time, it expects lenders will continue to tighten their underwriting, especially for specific sectors that become “overheated.”

Over the course of the year, Morgan Stanley noted that larger banks of more than $20 billion in assets tightened their lending standard much more than smaller banks. Multifamily loans had the greatest increase in net tightening and loan demand declined more in that category more than others in 2017.

On the positive side, LaSalle expects less hurdles for the major lending sectors in 2018 after the market overcame several potential obstacles in 2017, including the maturity of 2007 vintage loans, CMBS risk retention and Fed oversight of bank real estate.

As 2017 progressed, it became clear that risk retention wasn’t going to be a major market impediment, and issuance increased as the year went on, according to Kroll Bond Ratings Agency (KBRA). Transaction sizes, however, largely remained under $1 billion, which was partially attributable to risk retention that forced a number of originators to exit the market, as well as the size of the CMBS investor base.

On the up side of peaking property this year, KBRA noted, is that single borrower refinancing deals should continue to thrive as borrowers look to lock-in gains from property value increases. Borrowers may also want to lock in rates the Federal Reserve sending signals that more rate increases are to come in 2018.

As always, job growth will be a critical driver of real estate demand. And to the extent that the recently passed tax legislation that slashed corporate rates spurs additional business investment and hiring works as intended, job growth could exceed expectations.

“We’re now confronting a wider range of possible outcomes for the economy, depending on how various initiatives such as federal policy changes play out,” said Spencer Levy, CBRE Americas head of research and senior economic advisor, who added that agility will be more important than ever for investors this year.

Investors should shift to focusing on income gains rather than appreciation as their primary source of returns as cap rates flatten out or, in some cases, start to rise, Levy noted.

Major U.S. office markets are on the verge of a cyclical tipping point, with new construction and softening demand mirroring the evolution of previous CRE cycles, Moody’s Investors Service reported.

And while the markets may be hoping the supply-and-demand cycle plays out differently this time, that isn’t likely, Moody’s noted.

“New office construction is ramping up in many major U.S. cities, so that by the end of next year new inventory will be coming online at roughly double the rate of the past three years, while at the same time the growth of office-using employment will be slowing,” said Kevin Fagan, a Moody’s vice president and senior analyst.

As we enter 2018, there is 154.5 million square feet of new office space under construction, according to CoStar data. That compares to 97.8 million square feet delivered in 2017.

While the amount of office construction is increasing, the 252 million square feet delivered last year or under construction is still one-third lower than the 381 million square feet delivered in 2006 and 2007 when CRE markets last peaked.

However, underwritten office property values today far surpass those of the pre-financial crisis peak, particularly for CBD offices, Moody’s Fagan said.

Similar to the office market, new supply is also running high in the industrial property sector going into 2018 with 318.1 million square feet under construction following 311.6 million square feet delivered last year.

The big difference compared to office is that demand remains very robust for both bulk warehouse and closer-in delivery hubs as e-commerce continues to reshape and boost demand for distribution space. This positions the industrial market to perform well in 2018, although risks would escalate should economic growth slow, according to LaSalle.

While E-commerce is boosting the industrial investment potential, the retail sector continues to bear the brunt from lower traffic and sales. Construction of new retail space continues to decline with just 86 million square feet under construction at the beginning of 2018, well down from the 103.6 million square feet of retail space delivered last year.

Investors see exceptions within the sector, however. Grocery-anchored retail space in well-located centers remains in demand as reflected in the strong capital market activity at these centers that we believe will continue, according to LaSalle.

CBRE sees retailers and investors gravitating to either the discount and off-price sectors or luxury. This may create weakness, and, in many cases, investment opportunities, in secondary and suburban markets.