Supreme Court: NPN Investors Not Subject To Debt Collection Laws

Real Estate Note Buyers and Seller Carry Consultants

Advanced Technical Analysis of the Financial Markets

This past Thursday I had the distinct pleasure of spending 4 hours with Stan Harley, the publisher of The Harley Market Letter.![]() He shared some interesting insights in two canary in the mine real estate markets – Los Angeles and Phoenix and further detailed what can be expected for interest rates in the future. What was astonishing to me is just how powerful market cycles are and how they can be used to hedge one’s bets and to be proactive and not just reactive. Many of the seasoned real estate investors understand there are cycles to all business activity, but few understand simple analysis can be utilized to avoid game changing and unexpected shifts in the market place. Mr. Harley believes that even external events really have no bearing on the math.

He shared some interesting insights in two canary in the mine real estate markets – Los Angeles and Phoenix and further detailed what can be expected for interest rates in the future. What was astonishing to me is just how powerful market cycles are and how they can be used to hedge one’s bets and to be proactive and not just reactive. Many of the seasoned real estate investors understand there are cycles to all business activity, but few understand simple analysis can be utilized to avoid game changing and unexpected shifts in the market place. Mr. Harley believes that even external events really have no bearing on the math.

Most business strategists and real estate professionals failed to identify  the key pivotal turns for the housing market in 2006 and 2012. Market timing – as most are well-aware – is an extraordinarily difficult task. The foundation which underlies the basic principles of his analytical methodology is that market behavior can be described (and predicted) through a combination of simple cycles of differing periods. Cycles are the essential factor in determining how long a trend should run and when to expect reversals.

the key pivotal turns for the housing market in 2006 and 2012. Market timing – as most are well-aware – is an extraordinarily difficult task. The foundation which underlies the basic principles of his analytical methodology is that market behavior can be described (and predicted) through a combination of simple cycles of differing periods. Cycles are the essential factor in determining how long a trend should run and when to expect reversals.

“The knowledge and exploitatin of cycles embodies one of the most powerful analytical tools available for identifying trends and forecasting their reversale.” Stan Harley

CASE-SHILLER HOME PRICE INDEX

The Case-Shiller home price index tracks the value of residential real estate in 20  metropolitan regions across the United States. There are multiple Case-Shiller home price indices: A national home price index, a 20-city composite index, a 10-city composite index, and twenty individual metro area indices. The index is published on the last Tuesday of each month, with a two-month lag. The graph above depicts home price data from 1890 through the present. The lower graph reflects data for the Phoenix, AZ area region through Q3 2016.

metropolitan regions across the United States. There are multiple Case-Shiller home price indices: A national home price index, a 20-city composite index, a 10-city composite index, and twenty individual metro area indices. The index is published on the last Tuesday of each month, with a two-month lag. The graph above depicts home price data from 1890 through the present. The lower graph reflects data for the Phoenix, AZ area region through Q3 2016.

Data for the Phoenix region is somewhat limited compared to the national data as well as data for the southern California region. Because the economies of Arizona and Southern California are inextricialby linked – and the cyclical funcitons for both etch-out similar wave forms – a detailed analysis of the Los Angeles region can tell us alot about the market timing functions for the Phoenix area region . A cyclical analysis of the Los Angelia area region, the largest in the United States, is depicted below. Data for Phoenix and the rest of the country are very similiar.

. A cyclical analysis of the Los Angelia area region, the largest in the United States, is depicted below. Data for Phoenix and the rest of the country are very similiar.

(Editors note: I forwarded slides from the local AZ Real Estate Investors March market presentation(some of which were from the Cromford Report). Mr. Harley was not surprised they matched up.)

COMPOSITES ARE BACK TO THEIR WINTER OF 2007 LEVELS

Editors Comment–The Canary is in the coal mine.

HOME PRICES ARE PEAKING

Since his last review of the Case Shiller index Mr Harvey has revised his cyclical modeling to the numbers shown in the box above. The baseline cycle appears to be 196.8 months or 16.4 years. Notice how this cyclical function defined the June 1990 – Sept 2006 peaks and the March 1996 – February 2012 lows.

196.8 months or 16.4 years. Notice how this cyclical function defined the June 1990 – Sept 2006 peaks and the March 1996 – February 2012 lows.

The analysis points to a peak for the Los Angeles area – as well as the National Index overall – in the December 2016 time period. Because of the two month lag in the publishing of the data, we won’t know whether home prices have peaked for several more months. He also noted a narrowing in the range of the monthly price bars – a phenomenon that also occurred at the prior cyclical highs. However, based on the updaded data from the AZREIA slides for the period ending February, 2017, the trend is esclating.

At this point Stan Harvey is predicting a minimal drop of 12% in housing prices.

The Harry Dent team is suggesting a drop of 20% in housing prices.

Personally, I have noticed Days on Market are increasing. One of the local reps of a national title company here in Phoenix suggested they have seen a dramatic slowing in pricing for homes in central Phoenix.

Another title company rep noted their March has been VERY slow. A sales rep from a large local lender said their applications for March are way down.

Long term, Mr. Harley is predicting the big one in February, 2023

INTEREST RATES

Mr. Harley made one basic statement on interest rates. They will come down. Period.

HOW DOES THIS IMPACT NOTE BUYERS?

For note buyers keep your powder dry. Only buy notes with a strong equity position behind them. Another words be patient, and buy notes with a loan to value of less than 70%, preferrably less than 65% – all of which is subjective to mitigating factors. If one maintains that cardinal principal, then even with a potential property value drop of 20%, the chances of a payor walking are minimal.

HOW DOES THIS IMPACT NOTE SELLERS?

Make sure you get at a minimum of 10% down, preferrable 15% – 20% down from your buyer. Continue to require at least an 8% interest rate on your note from your buyer–preferrable 10%, but stay in line with the Dodd-Frank Act requirements. There are multiple posts regarding The Dodd-Frank Act on this site.

HOW DOES THIS IMPACT IRA INVESTORS?

It is all positive. Be conservative and positive. If market interest rates drop as forecasted, seller financed notes continue to be a rewarding investment alternative.

PS–It is all about being proactive and NOT reactive. Alot of money can be made in a down cycle–more than in an up cycle.

It is not unusual for a note holed to sell their note to get a certain amount of cash. But………….when given a quote by a note buyer many time they are shocked at the huge discount and insulted—maybe even angry that a note broker or buyer would try to “steal” their “good” paying note. Any proficient note buyer / broker will offer alternatives in the form of quoting to buy a piece or just some of the outstanding balance. Have you ever bought a full pizza? Have you ever bought just a few pieces of piz za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

Sometimes as a note owner you only need a specific amount of cash. Selling the whole note makes no cents. There are multiple ways to architect a partial sale. You can sell 12, 24, 60,100 or however many of payments to bring you the cash your need. For the next x# of months, those payments would go to the partial note buyer. After the buyer is paid back, the remaining payments would revert back to you.

Selling a partial gives the note seller a great amount of flexibility. Partials are always a great tool to use when the note holder has an immediate cash requirement and only needs a specific amount of money to cover a specific situation or for a specific purpose. A partial minimizes the discount and frees up cash. It is the best of the best. The terms of the note remain the same for the note payor/borrower. The only thing that changes is the payments are directed to the third party servicing company. Additionally there is contractual language giving the partial buyer the right of first refusal to buy additional payments if they so choose.

What about an early payoff?

Many notes do pay off early. The average time a house or note is paid off historically is 7 – 10 years. If it is paid off early, there are contractual agreements / documents from the outset that are managed by the third party note servicing company determining the payoff and or re-conveyance.

What if the note goes into default?

Unfortunately some notes/mortgages do go into default. IT is a realty of the financial world. If in fact that happens, the contractual agreement spells out the options. Either a buy back from the partial buyer or proceed with the foreclosure /eviction process with the goal of taking back the property and resell it for fair market value. Both the original note buyer and the partial buyer benefit. The partial buyer is made whole with the balance going to the original note seller.

Three Real Life Case Studies

Houston, TX 11/30/15 – Single Family house

Gerry owned a note on a single family house in a so-so area of Houston. He needed money for some personal issues and needed help. I offered to buy the full at a larger discount due to the issues noted below. He was not real enthused with the offer, so we agreed to a partial purchase.

Deal Points

Good Points

Gerry negotiated a great terms with a sort-of strong buyer. Meaning the buyer put down a very strong $14,000 on a $60,000 purchase resulting in a great Loan to Value(LTV). The 7% interest rate was OK. It had a relatively short amortization period of 60 months with a great on time pay history. The 3 Buyer’s FICO scores were weak, but they had a good job history.

Marginal Points

Due to the drop in oil, Houston lost 44,000 jobs. The neighborhood had some marginal houses, but in the process of changing for the good. For these two items, if felt uncomfortable with a full purchase.

Bottom Line

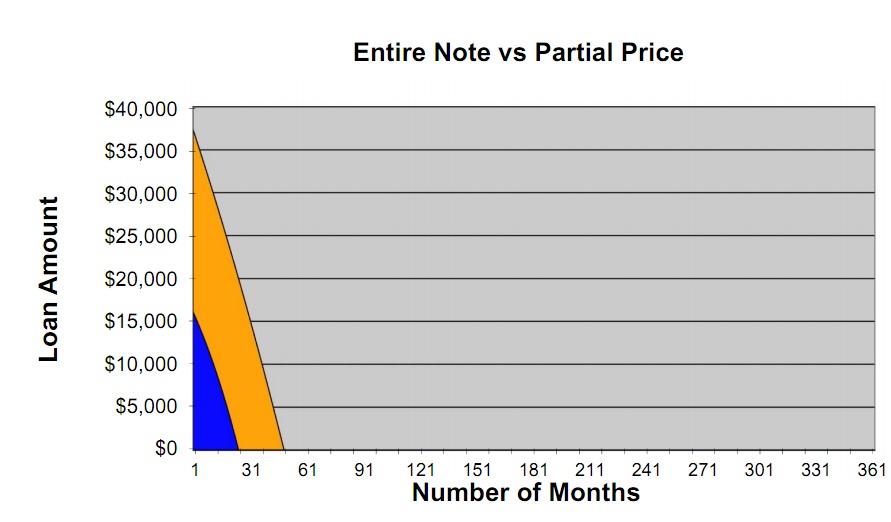

We bought a 24 month partial with the option to purchase the balance in 15 months. It was a secure, safe purchase and Gerry received what he needed. Out Investment to Value was a very secure 26% with a safe Loan to Value of 57%. The graph depicts what we purchased(blue) and what the seller kept. Within one year we bought the gold portion all in our IRA.

Fast forward 11/30/16

Gerry called requesting if Capstone would be interested in purchasing the balance of his note. He had a lingering debt situation. After a short due diligence period, we closed within 10 days. Again Gerry was happy and we were happy owning the full note. Three weeks later we sold the full note to one of our Note Investor Forum Meetup attendees for his ROTH IRA.

Summary

The note seller had a situation, we provided him a solution—twice. The Meetup attendee was in his early 70’s. He wanted a higher yielding note with a shorter amortization period. This was his first note purchase. He is excited to buy additional opportunities.

_____________________________________________________________

Salem, OR 12/20/16 – Land Parcel

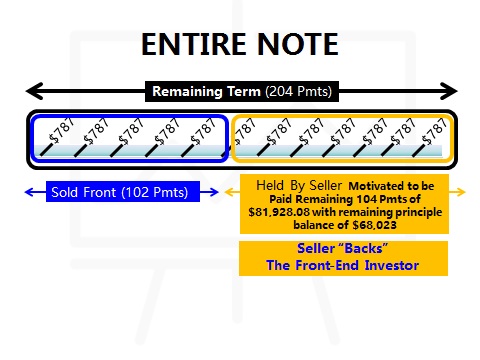

A note colleague referred his friend Kirt his client, Joyce who owned a 13.17  acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

Deal Points

Good Points

Joyce’s buyer had a very good job as a helicopter pilot earning close to $150,000/yr. The servicing company provided a very stable 36 month payment history. She also had a survey of the land which had all utilities. Most likely in the future the apartment complex would expand—buying out the pilot and our partial.

Marginal Points

Joyce did not negotiate good note terms. Only a 4% interest rate (her realtor said that was fair). In reality for land it should have been at least 10%.

Bottom Line

We bought a 102 month partial with the option to purchase the balance in the future. It was a secure, safe purchase and Joyce received the funds she needed. We had a very strong ITV of 11% . It was a true win-win. Our referral partner received a referral fee and sold some gold to Joyce. Joyce was able to buy her house and the Capstone investor had a very safe and secure partial note investment in her mothers’ IRA.

Fast forward 4/5/17

Joyce called stating that she wanted to sell the remaining 102 payments ($68,023) which we did for $19,377. She did not want to wait 102 months to cash out the remaining payments. Joyce got what she needed and we received a fair deal. On the entire transaction, our Investment To Value (ITV) was a very safe 17%, in a fast appreciating real estate market. The odds are high the parcel will be sold for development in the near future providing the investor a very nice return because she bought the note at a steep, but fair discount due to the 4% note rate.

Summary

What really happened though is even more normal. Joyce calls back wanting sell the rest of the back-side far before the re-assignment period. Many not sellers buy into a partial transaction because the transaction mitigates the discount. But…………..more often than not, they will want to sell the remaining balance early to meet life needs.

Partials are a unique method of meeting many needs for note buyers and sellers. They should not be over looked. It is an incredible passive investment vehicle for your ROTH IRA

This Case study was/will be presented at the Note Investors Summit April 5-7, 2018 in Irvine, CA

Emotional equity mitigates the risk in the note buying process. There three types of notes in this business are of three types which come in the form of high equity, partial equity, a nd no equity notes. Majority of the note buyers contemplate on the more obvious profits, without giving any consideration to the possibility of profits coming from emotional attachment. Emotional Equity. Many times the forgotten and sometime the most important attribute to consider when purchasing a note.

nd no equity notes. Majority of the note buyers contemplate on the more obvious profits, without giving any consideration to the possibility of profits coming from emotional attachment. Emotional Equity. Many times the forgotten and sometime the most important attribute to consider when purchasing a note.

People were used to buying equity covered deals during 2007 so that in the event that the homeowner makes the decision not to pay any longer, they would have the option of foreclosing and recouping their money while making profit at the same time. Nonetheless, with the housing market crash in which most of the home values were wiped out, the disappearance of those equity notes began. Any attempt to purchase them now will result in paying a premium. This is why it is a wise decision to have the positives to every kind of note taken into consideration. It is worthy to note that purchasing equity against no equity deals is the fact of no-equities being cheaper, yet the upside potentials of the two are identical.

Note Buyers, Homeowners, and Emotional Equity

The fact that homeowners have no concept regarding the worth of their houses and that majority of them are not really interested to know since the houses are theirs anyway, which is most important, are the two things that must be put into consideration before purchasing notes. The majority of homeowners have no interest in leaving their houses, considering the fact that these homes are the places they grew up in, and as such, have lots of memories there. Also, these houses have enough space to contain the entire family. Many of these families have lots of kids that cannot just be uprooted and move them to somewhere else, since such thing could be very difficult to cope with. One who is a note buyer must keep certain things in mind such as details of homeowners having the tendency to continue holding on when it comes to certain things, thereby making it imperative for them to keep on holding to their houses. Note buyers have great opportunity here if there a willingness on their part to take the risk and have things worked out with the homeowners since they will always refuse to vacate their homes. This may be the time for investors to exert effort in carving out plans for homeowners to take into consideration. A no equity deal can benefit both parties, for the fact that the investors will receive monthly payments while simultaneously have the latitude of structuring terms that would favor homeowners.

Nonetheless, it is not only nostalgia that sometimes makes it difficult for homeowners to vacate. Expenses play important role as well. For a party of seven, for example, renting an apartment would prove even more expensive and inconvenient for them. Again residing in an apartment might not be a viable option especially in cases where the homeowner has pets. Matters like these motive homeowners to either look for additional work or demand for a higher income so as to retain their homes and avert foreclosure.

It is for these reasons that note buyers should weigh and make analysis of all probabilities. The perfect note does not really exist. Sometimes people miss an opportunity to make profits just because they want to avoid risks. Have a second thought over this! Emotional Equity is a very important ingredient of the note buying process.

Which is the best approach to analyze a note for the amount of the discount; collateral or yield? While both are important, there are three factors to consider when purchasing a note:

LTV is the ratio of the note balance to the value of the property. For example, a $100,000 property that sells with 5% down and a $95,000 note balance has an LTV of 95%. The higher the LTV, the higher the risk of the note. Why? Because a high LTV at the initiation of a mortgage indicates how much “skin in the game” the mortgagor has put at risk. To put it in perspective, if a property buyer puts only 5% down on the purchase of a property and borrows the remainder, who is taking the bigger risk; the buyer who has only $5,000 at risk, or the note holder who has $95,000 at risk, with collateral of only $100,000?

Let’s take this scenario into the future ten years where the note has been paid down to $83,000. What is the LTV? 83%, right? Now who has the more at risk, the mortgagor or note holder? Since the mortgagor now has $17,000 equity, as opposed to the original $5,000, the probability the mortgagor will just walk away is reduced.

More importantly, since there is ten years of seasoning, the mortgagor has accumulated what is called “emotional equity” or “psychological attachment”; meaning the mortgagor has established roots in the community, in schools and employment. The chances of the mortgager just packing up and leaving are much less.

An offer based on yield will differ from an offer based on ITV.

Which one should you make?

In other words, even though the property buyer put only 5% down, as time went on, he or she accumulated equity, as well as demonstrating to a note buyer that they are a safer risk now than ten years earlier when they had virtually no risk because of the small down payment, no equity and no roots in the community.

Contrast this to a buyer who puts $20,000 or 20% down on a $100,000 house, with an $80,000 note balance. The LTV is now 80%. The buyer has $20,000 invested in the property. Not only do they have “skin in the game”, but should they get into trouble, they will have more of an opportunity to sell the property to get some, if not all of their investment back. Add to this that the note holder’s collateral is higher with an 80% LTV, than a 95% LTV. In other words, the note holder taking less of risk, and the buyer is taking more of the risk.

Why LTV Matters To A Note Investor

For a note investor, the LTV indicates the amount of “skin in the game” a property buyer put at risk at the origination. As time moves on, the LTV reflects the monetary equity the buyer has accumulated, as well as emotional attachment they have in the property.

With this in mind, let’s examine ITV, or investment-to-value. ITV is the amount a note buyer invested in the note divided by the “as is” value of the property.

To minimize the note investor’s risk, ITV is often tied to the credit score, down payment and property value.

Remember, the only real protection a note investor has is the collateral, or value of the property in the event of default. Since we know the collateral can be devalued by market conditions( the 2008 melt down) and/or deterioration of the property, ITV is very important to the amount of the discount a note buyer requires.

In the above case study, let’s assume the house sold for $100,000 with 5% down, and a $95,000 mortgage at 8% for 30 years, with payments of $697.08. Let’s further assume the mortgagor’s credit scores are in the low 600s. Because of the low credit scores and low down payments, a note investor requires a 65% ITV and at least an 11% yield. What will the investor offer?

For a 65% ITV he would pay $65,000 (65% of $100,000).

To receive an 11% yield a note investor would pay $73,197.

Since the offers are quite different, which one will the note buyer favor?

The note buyer will favor the $65,000 offer.

Rule Of Thumb

An investor should make the offer that gives the note investor the acceptable ITV or yield, WHICHEVER IS LOWER.

In conclusion; LTV tells a note buyer how much “skin in the game” the mortgagor has, or how much monetary or emotional attachment they have in the property.

ITV, on the other hand, tells the note investor how much he or she will invest in the note in relation to the value of the property. Yield is determined by the best and safest use of the note buyer’s money.

The amount of the mortgagor has invested, along with the value of the collateral and their credit score, will determine the ITV of the note buyer. Yield is the rate of return a note buyer demands when considering mortgagors’ credit, property value, and mortgagor’s equity and other risks. When applying LTV, ITV and yield to the purchase of a note, all three are important and should be tied to one another. In other words, the down payment, credit score, value of the property, equity in property should be tied to the ITV and yield a note investor demands.

The more risk an investor incurs because of high LTV, the lower must be the ITV, and the yield must be higher. The note buyer will offer the lesser of the ITV vs. yield.

So, which is most important, LTV, ITV or yield?

The answer is that all are important and interrelate to one another.

Yield is determined by the best and safest

use of the note investor’s money. BUT….

YIELD IS NOT REALIZED UNTIL THE NOTE IS PAID OFF.

The above article was reprinted with permission from The Paper Source newsletter—January, 2017 edition. Tom Henderson, the author, has been buying notes and real estate since the 1980s. He is president of H&P Capital Investments, LLC, which buys, sells and trades owner financed notes.

Hedge fund manager and former Goldman Sachs partner Steven Mnuchin  confirmed to CNBC on Wednesday morning that President-elect Donald Trump has nominated him for the position of Secretary of the U.S. Department of the Treasury.

confirmed to CNBC on Wednesday morning that President-elect Donald Trump has nominated him for the position of Secretary of the U.S. Department of the Treasury.

Trump’s choice of Mnuchin, 53, who served as the President-elect’s national finance chairman during his campaign, is considered controversial because Mnuchin has never worked in government and his roots in Wall Street would seem to conflict with Trump’s anti-financial industry sentiment during his campaign.

One area where he does agree with Trump, however, is the need for reduced regulation. Mnuchin laid out a number of his initiatives on CNBC’s Squawk Box, should the U.S. Senate confirm him as the 77th Treasury Secretary. One of those is to roll back the Dodd-Frank Wall Street Reform and Consumer Protection Act, which passed in 2010 and is considered by the Obama Administration to be one of its greatest achievements. In various speeches and interviews throughout his campaign and since his election, Trump has vowed to overhaul the controversial financial reform law.

“We (Mnuchin and Trump’s choice for head of the U.S. Department of Commerce, Wilbur Ross, also announced on Wednesday) have been in the business of regional banking, and we understand what it is to make loans,” Mnuchin told CNBC. “That’s the engine of growth to small- and medium-sized businesses. The number one problem with Dodd-Frank is it’s way too complicated and it cuts back lending. So we want to strip back parts of Dodd-Frank that prevent banks from lending, and that’ll be the number one priority on the regulatory side.”

Mnuchin told CNBC that the U.S. economy can sustain a growth level of between 3 and 4 percent. In fact, he called sustained economic growth “our most important priority.”

“It is absolutely critical for the country,” Mnuchin said. “We absolutely can have sustained growth at that level. To get there, our number one priority is tax reform. This will be the largest tax change since Reagan. We’ve talked about this during the campaign. Wilbur and I have worked very closely together on the campaign. We’re going to cut corporate taxes, which will bring huge amounts of jobs back to the United States. We’re going to get to 15 percent, and we’re going to bring a lot of cash back into the U.S.”

In an interview with Fox Business after the announcement of his nomination, Mnuchin said he believes that the controversial government conservatorship of Fannie Mae and Freddie Mac should end and that the private market should have more of a share in the mortgage market.

“We will make sure that when they are restructured, they are absolutely safe and don’t get taken over again. But we’ve got to get them out of government control,” Mnuchin said, according to Bloomberg.

“A resolution of the conservatorship of Fannie and Freddie appears likely with Mnuchin as Treasury secretary,” says Tim Rood, Chairman of The Collingwood Group. “His experiences at Dune Capital, particularly the IndyMac/OneWest purchase and turn around, will most certainly influence his decision-making calculus.”

Five Star Institute President and CEO Ed Delgado said of the nomination of Mnuchin for Treasury Secretary: “I anticipate that with this new appointment, Treasury will continue to promote the department’s mission by encouraging a strong economy and creating economic growth and stability. As the economy further recovers from the Great Recession it is imperative that the housing industry and Treasury work in hand and hand to ensure housing and economic prosperity.”

Mnuchin left Goldman Sachs in 2002 after 17 years with the global investment banking firm to become vice chairman of hedge fund ESL, and he later became CEO of another hedge fund, SFM Capital Management. In 2009, Mnuchin and a group of investors purchased the failed Pasadena-based IndyMac bank from the FDIC for $1.5 billion after the mortgage meltdown and renamed the bank OneWest. In the years immediately following the crisis, OneWest’s foreclosure practices generated considerable controversy, particularly in California.

Mnuchin’s hedge fund, Dune Capital Management, of which he currently serves as CEO, became involved in Hollywood motion pictures years ago, financing such box office hits as “X-Men” and “Avatar.”

“If he gets the post, Mnuchin will bring a lot of mortgage expertise to the Treasury Department,” says Rick Roque, President of Menlo. “He bought Indymac, renamed it OneWest and then sold that company to CIT Group in 2015. That kind of experience, in addition to his experience in sub-prime origination, retail origination, and correspondent channels will prove to be very valuable to the non-depository mortgage banking market.”

The Consumer Financial Protection Bureau is likely to be reigned in if not rendered i mpotent or even abolished under President Trump. He has said he would come “close to dismantling” it along with Dodd-Frank. That is good news for small business, consumers, the economy in general — and note investors.

mpotent or even abolished under President Trump. He has said he would come “close to dismantling” it along with Dodd-Frank. That is good news for small business, consumers, the economy in general — and note investors.

The CFPB is the brainchild of super-liberal Massachusetts Sen. Elizabeth “Pocahontas” Warren, who never met a business she doesn’t want to regulate.

“At stake is the agency’s aggressive approach to regulating credit and prepaid cards, mortgages, payday and student loans, debt collection, credit reporting and other areas of consumer finance since opening for business in 2011.”

WASHINGTON, Nov. 11, 2016 — Donald Trump has taken the first step to fulfill his campaign promise to “dismantle” Dodd-Frank and the Consumer Financial Protection Bureau. He is considering one of the leading critics of Dodd-Frank on Capitol Hill, Rep. Jeb Hensarling, as Treasury Secretary.

Mr. Hensarling last year laid out a blueprint for replacing Dodd-Frank that many observers view as a starting point. In an interview Thursday, he said the Trump team’s statement “is music to my ears,” and that he planned to make the bill, dubbed the Financial CHOICE Act, his top priority next year.

He said he had spoken with Mr. Trump’s team about the matter in the past, adding: “I think they like the thrust of the legislation and many major components of it.”

As for the prospect of him taking the Treasury slot, the Texas lawmaker said he would “certainly have the discussion” if the Trump administration comes calling, “but I’m not anticipating the telephone call.”

The transition team’s blueprint on the president-elect’s website states that the Trump team “will be working to dismantle the Dodd-Frank Act and replace it with new policies to encourage economic growth and job creation.”

The president-elect has tapped Paul Atkins, a former Republican member of the Securities and Exchange Commission and longtime Dodd-Frank critic, to recommend policies on financial regulation. An aide to Mr. Atkins, who heads a financial regulation consulting firm, referred requests for comment to the Trump transition team, which couldn’t be reached.

Mr. Hensarling’s bill is built around a trade-off: Banks can free themselves from various regulations, such as tough stress testing, as long as they maintain capital equal to at least 10% of total assets and high ratings from their regulator.

That would immediately help many small locally focused banks that tend to be better capitalized, but not necessarily megabanks with sprawling international operations that generally have capital levels below that level.

In the interview, Mr. Hensarling said he would try to convince Mr. Trump’s team to support his approach instead of their campaign-trail promise to reinstate the Depression-era Glass-Steagall law separating traditional lending from investment banking.

Mr. Hensarling’s bill also would make other significant changes, such as requiring that many financial regulations be subject to cost-benefit analysis for the first time and tying the budgets of regulatory agencies, including the CFPB, to congressional appropriations.

The CFPB has enjoyed a high level of independence by getting its funds from revenues insulated from the legislative process.

It is possible Senate Democrats could seek to block GOP efforts they view as overreach, but lobbyists and congressional aides are optimistic that some moderate Democrats up for re-election in 2018 in states that voted for Mr. Trump will be inclined to compromise. Republicans also may come under pressure to change the Senate rules to ease passage of controversial legislation, but it is far from clear they would make that move.

Our take:

The proposed Seller Finance Enhancement Act – HR 5301…, an amendment to the Dodd/Frank legistation is way over due

This bill rolls back some of the excessive regulations of Dodd/Frank by allowing Seller Financed transactions to expand from 3 in a rolling 12 month period to 24 in a year.

While this is not a massive change, it will provide significant relief for the vast number of real estate investors who choose to seller finance property.

Dave Franecki

Unlike the late night real estate infomercials where the alleged “gurus” will teach you their great strategies for 100% leverage and how “you too can buy fantastic real estate for no money down”, small business sales are not done that way. While leverage plays a role, buyers have to come to the table with a deposit. For an individual buyer with limited resources, the risk can be great and that concern, coupled with few available lending sources, has meant that seller-financed deals is the norm in these size deals.Jim Sinclair, Senior Vice President of Murphy Business & Financial Corporation LLC, a national business broker and M & A firm, advises his seller clients to “act like a bank if they are going to offer financing to the buyer.” To this end, he urges them to do a thorough background and credit check on the buyers. Sinclair says that while deals vary greatly, “under the right scenario, a buyer can expect the seller to carry a maximum of 50% of the total purchase price as a balance of sale.”

Unlike the late night real estate infomercials where the alleged “gurus” will teach you their great strategies for 100% leverage and how “you too can buy fantastic real estate for no money down”, small business sales are not done that way. While leverage plays a role, buyers have to come to the table with a deposit. For an individual buyer with limited resources, the risk can be great and that concern, coupled with few available lending sources, has meant that seller-financed deals is the norm in these size deals.Jim Sinclair, Senior Vice President of Murphy Business & Financial Corporation LLC, a national business broker and M & A firm, advises his seller clients to “act like a bank if they are going to offer financing to the buyer.” To this end, he urges them to do a thorough background and credit check on the buyers. Sinclair says that while deals vary greatly, “under the right scenario, a buyer can expect the seller to carry a maximum of 50% of the total purchase price as a balance of sale.”One major change Sinclair has seen recently is that several banks have lowered their minimum deal size from $500,000 to around $350,000. This is great news for individual buyers as they now have another option where none existed before.

Once the deal size starts to increase, the percentages and amounts that banks will contribute increases commensurately. The most common form of bank financing to individual business buyers has been from those institutions participating in the Small Business Administration’s 7(a) loan program. Under the SBA umbrella, the government guarantees a percentage of the loan that a bank will make. There is very specific criteria regarding the SBA 7(a) program eligibility and collateral guidelines, and while the government essentially guarantees part of the loan, the banks must be in compliance and the buyers must meet other specific guidelines.

John Martinka, of Martinka Consulting, a Washington state mid-market mergers and acquisitions firm, was involved in a deal recently representing the buyer in the purchase of a Washington-based fabrication business. In that deal, “a competing buyer to his client could not get approved for financing and the suspicion is he would not personally guarantee the loan or put up his house” as collateral.” Martinka also explained that “relevant business experience, meaning some management experience by the buyer is a requirement.”Martinka is typically involved in deals under $10.0 million and regardless of the percentage of bank financing, he notes that a portion of all of the deals include some participation by the seller in the financing. In other words, the banks want to see the seller absorbing some of the risk as well.

While banks may be softening their stance regarding deal size, buyers cannot escape having to be qualified financially and experience-wise, and must be willing to personally guarantee the loan. This is also the case with seller-based financing although in these instances, while personal guarantees are required, the assets of the business, rather than personal ones, are usually pledged by the buyer. Similarly, when selling a business, the owners need to realize that they are going to have to participate in the financing to some extent. The smaller the deal; the more they have to fund it. While every seller would obviously would prefer an all-cash deal, those deal terms are not common. No matter how badly the parties want to do a deal, both sides need to keep an open mind regarding the financing terms because nothing gets done without funding.

http://www.forbes.com/sites/richardparker/2016/09/27/financing-a-business-acquisition-banks-lower-threshold-by-up-to-30/#3983c3ded636

Acquiring income producing property is one of the best ways to create wealth and achieve one’s long  term financial objectives. However, at some point, many investors tire of managing their properties. If you are an absentee landlord, this may experience this soone r than later. Of course the natural question is…. if owning real estate is not as glamorous or as easy as is promoted, what else does one do to create wealth? The stock market? Well maybe not—this year’s average returns are roughly 2% with a lot of risk like playing in a casino.

term financial objectives. However, at some point, many investors tire of managing their properties. If you are an absentee landlord, this may experience this soone r than later. Of course the natural question is…. if owning real estate is not as glamorous or as easy as is promoted, what else does one do to create wealth? The stock market? Well maybe not—this year’s average returns are roughly 2% with a lot of risk like playing in a casino.

For example two seasoned investor friends bought several lower price band rental properties in Birmingham, Chicago, Indianapolis and Milwaukee. They were convinced their target 20% cap rate was very a reasonable. Now after 2 years, multiple property managers, handymen, evictions, code violations, phantom tenants etc, they saw their very easy projected cap rate drop to more like 6-7%. The stress, worry and frustration really began to take their toll.

Friend #1, Jason, decided to just bail and sell. He is putting his money into group foster homes. If professionally operated he will generate a serious return and satisfy his passion-to help kids, get his wife out of work, not to mention the serious cash flow. Friend #2, Dan, has decided to sell his properties and be the bank with seller financing. He decided to turn all the tenant worries into mail box money. He doesn’t want a job, just the cash flow.

Dan and I discussed the variables. As a seasoned note guy and seller carry consultant I made several  recommendations to Dan on how to structure the transactions. We discussed the pros and cons. How to structure the transaction– to make a long term play with minimal risk. I was able to utilize my years of real estate experience and note structuring basics to demonstrate to him how, if structured properly he could generate a safe and reliable 10%+ return on his investment. A quantifiable and predictable rate of return.

recommendations to Dan on how to structure the transactions. We discussed the pros and cons. How to structure the transaction– to make a long term play with minimal risk. I was able to utilize my years of real estate experience and note structuring basics to demonstrate to him how, if structured properly he could generate a safe and reliable 10%+ return on his investment. A quantifiable and predictable rate of return.

When structuring a seller carry back, Dan is taking a very proactive approach—focusing on six primary underwriting areas. While his goal is to quickly sell his rentals, above market pricing, he wants to mitigate risk and maximize his return and still keep his options open in the event he wants to sell his  seller carry back note in the future and avoid a deep discount(haircut) on the note resale. He is not just selling to anyone with a pulse thus minimizing risk and no stress .

seller carry back note in the future and avoid a deep discount(haircut) on the note resale. He is not just selling to anyone with a pulse thus minimizing risk and no stress .

Dan is implementing the following underwriting criteria.

The net result is:

Buyer defaulted? Take it back and sell again.

When it is all said and done, which is better a rental or a note?

Seller financing is an under utilized tool and is here to stay.

Dave Franecki is the Fund Manager of Capstone Capital USA.

Capstone Capital USA focuses on acquiring Performing and Re-performing 1st position notes and structuring seller financed transactions.

{kind=link}