https://www.youtube.com/watch?v=Q68tqYQiu2g

Real Estate Note Buyers and Seller Carry Consultants

Editors Note: The following was written by Michael Maharrey and appeared in shiffgold.com.

While is is written by the Gold expert Peter Schiff, the principles, the overlay is expressed as to what is really going on in peoples thought processes.

Bottom line change is in the wind. JPMorgan Chase boss Jamie Dimon urged investors Wednesday to prepare themselves for turbulence in the market in the weeks ahead – warning that extraordinary financial circumstances were creating a potential “hurricane” for the economy.

“It’s a hurricane. Right now, it’s kind of sunny, things are doing fine, everyone thinks the Fed can handle this,” Dimon said during a conference sponsored by AllianceBernstein, according to Bloomberg.

“That hurricane is right out there, down the road, coming our way,” he added. “We just don’t know if it’s a minor one or Superstorm Sandy or Andrew or something like that. You better brace yourself.”

We cannot hide from what is coming. My question to you is, ” Do you have the financial resources if your note payor stops paying? What is your backup plan? Capstone Capital USA has the resources to provide you a lump settlement for all or for a portion of your seller financed mortgage. We will provide a fair market FREE quotation.

Doesn’t it make sense to be proactive while the payor is still current with their payments vs being late causing you to market a note with a developing  poor pay history? Read on…I believe you may identify with the following narrative……….

poor pay history? Read on…I believe you may identify with the following narrative……….

_________________________

Average people are worried about the economy. Consumer confidence has been falling. People undoubtedly feel the squeeze of inflation. But despite their general discontent, most people don’t seem to think a severe economic downturn is imminent — despite many warning signs.

Why not?

Peter Schiff has been warning that a recession is in all likelihood already here. In a recent interview on NTD News, he emphasized that the economic downturn will be much deeper than anybody expects.

I don’t think it’s going to be a mild recession. I think this recession is going to be worse than the Great Recession that started following the 2008 financial crisis.”

But most people remain sanguine about the economy. They may fret a bit about ongoing inflation – as reflected in the consumer sentiment numbers – but they assume the Fed will be able to tame the inflation dragon with some modest monetary tightening. They even concede this might cause a minor recession, but the mainstream believes Jerome Powell when he claims the economy is strong enough to handle higher interest rates and some balance sheet reduction. Virtually nobody besides Schiff and a few other contrarians sees anything major economic problems coming down the pike.

But as Schiff pointed out in that same interview, nobody saw the 2008 recession coming either.

In fact, when we were six or seven months into that recession, the Federal Reserve and other economists still claimed that there was no recession anywhere in sight. So, this recession is going to be much worse than that one.”

In retrospect, the signs of a housing crash were pretty obvious in 2006 and early 2007. It was apparent that there were serious problems in early ’08. But almost nobody in the mainstream saw the financial crisis and Great Recession coming. Like today, there were only a few voices in the wilderness sounding a warning.

Why is it that so few people are prepared for economic crashes when the warning signs are so obvious?

There are certainly many factors, but one likely reason people don’t can’t see the train hurtling down the tracks is a psychological phenomenon known as “normalcy bias.”

In a nutshell, normalcy bias is a form of denial based on the assumption that everything will continue as normal. Bocoran pola gacor hari ini.

Here’s a more formal definition.

Normalcy bias is a psychological state of denial people enter in the event of a disaster, as a result of which they underestimate the possibility of the disaster actually happening, and its effects on their life and property. Their denial is based on the assumption that if the disaster has not occurred until now, it will never occur.”

In simple terms, it’s the “it can’t happen to me (or us)” syndrome.

Normalcy bias leads to inaction. It’s one of the reasons people often ignore hurricane warnings. The assumption is “we haven’t ever had a hurricane yet, and if we do, it probably won’t be that bad.”

According to PsycholoGenie, there may be some evolutionary basis for normalcy bias.

There is a theory that associates normalcy bias with the evolutionary aspect, that suggests that paralysis gives an animal a better chance of survival because predators are less likely to attack and feed on something that isn’t moving.”

That’s great if predators are hunting you in the jungle. It’s not so great if an economic disaster is looming.

I think normalcy bias is one of the reasons the Federal Reserve’s transitory inflation narrative gained so much traction. Despite the money printing after the 2008 financial crisis, consumer prices never rose as many predicted. Instead, inflation manifested in asset prices, particularly stocks and real estate. This led Fed policymakers to assume they could do quantitative easing again – and even double down on it – without severely impacting consumer prices. Of course, the dynamics were different during the pandemic. Not only was the Federal Reserve printing trillions of dollars, but the US government was also handing out cash in the form of stimulus checks, even as most Americans were sitting at home producing nothing. This was a recipe for rapidly rising consumer prices.

But normalcy bias kicked in. We were told, “Inflation didn’t happen before, so don’t worry, it won’t happen now.” An assumption set in – things will continue as they always have. And when prices started to spike, these same people assured us that it was transitory. All along, Schiff was warning that inflation wasn’t transitory. But pretty much nobody listened.

Similarly, I think normalcy bias has played a role in gold and silver’s lackluster performance in recent months. As Schiff put it in a video on the recent performance of gold, “Even though we have a lot of inflation today, investors still think we won’t have inflation tomorrow.”

Because the Fed has been able to raise interest rates to keep inflation at bay in the past, the mainstream just assumes it will be able to modestly raise rates and keep inflation at bay this time around. Never mind that there are different dynamics in play and plenty of signs that inflation will likely remain entrenched over the coming months. Normalcy bias has blinded people to the fact that it would require a Paul Volker style hike to push real interest rates into positive territory — the only cure for inflation.

At some point, reality will cut through the normalcy bias. It always does. But when the mainstream wakes up, it’s too late.

As you survey the economic landscape, be aware of normalcy bias. There is no reason to assume things will continue as they always have. Keep your eyes on the economic data, analyze it objectively and keep basic economic principles in mind. And then, prepare accordingly.

Dave Franecki originally wrote this article which was published in the March 2021 NOTEWORTHY NEWSLETTER

Whether you are a seasoned real estate / note investor or a new to the note space, buckle up as this article addresses both audiences. Do you see what is happening as inflation or deflation in the next 3 years? This article will focus on inflation therefore a weaker dollar vs deflation and a stronger dollar.

We are entering the most turbulent period in US financial history…

That’s because severe crises are brewing on multiple fronts and are converging. There’s going to be much less stability of any kind—financial, economic, political, social, cultural, or military—in the months to come. The whole system will have a complete reset, and soon. We’re in an economic no-man’s-land…

There is a stock market bubble, a real estate bubble, a bond super-bubble…

Visit My Page : Sundulqq

It’s really an Everything Bubble. The coming financial volatility will be unlike anything we’ve ever seen before… It could be the BIGGEST thing not just since the Great Depression of 1929 to 1946. It could be the BIGGEST thing since the founding of the USA. The enormous and unprecedented effects of this have only just begun. Almost EVERYONE could lose money in the ensuing economic collapse. The question is how much. That means most investments YOU own are likely overvalued and high risk.

How did this happen?

In a desperate attempt to paper over their problems, governments have printed trillions of new currency units, brought interest rates to below zero, and bailed out failing institutions.

But those gimmicks have now been exhausted. We are in the beginning of the GREAT RESET. Nobody has ever seen a market so good and so bad at the same time. This black swan has a split personality!

The top layer of the data onion looks good. But the more layers you peel off the smellier it gets, and the more you’ll want to cry. On the surface, things are looking good. But in the deeper layers of data, the current state of the industry shows some major red flags. And the deeper you look, the future of the industry looks downright scary. Investing basics have gone by the wayside because of the fear of missing out for [more].

How does this inflationary time impact notes as a passive investment?

A “set it and forget it” buy and hold passive note investor a is typically in for the long term yield. They want the 10+ year run of “guaranteed returns”. It feels good. But, inflation, the eroding of the dollar’s purchasing power over time erodes those payments just as it has since 1913.

a is typically in for the long term yield. They want the 10+ year run of “guaranteed returns”. It feels good. But, inflation, the eroding of the dollar’s purchasing power over time erodes those payments just as it has since 1913.

Ask yourself this question. Today, if you spent $1,000 at WALMART, how many carts of groceries would that buy as compared to ten years ago? A huge difference. What about in 3 years ago? With just food prices escalating, it may be safe to assume a 20% drop in buying power with all the funny money being pumped into the system. Find todays real inflation #’s here.

The Wolf Report had a great article on this subject. The Dollar’s Purchasing Power Dwindles to Another Record Low.

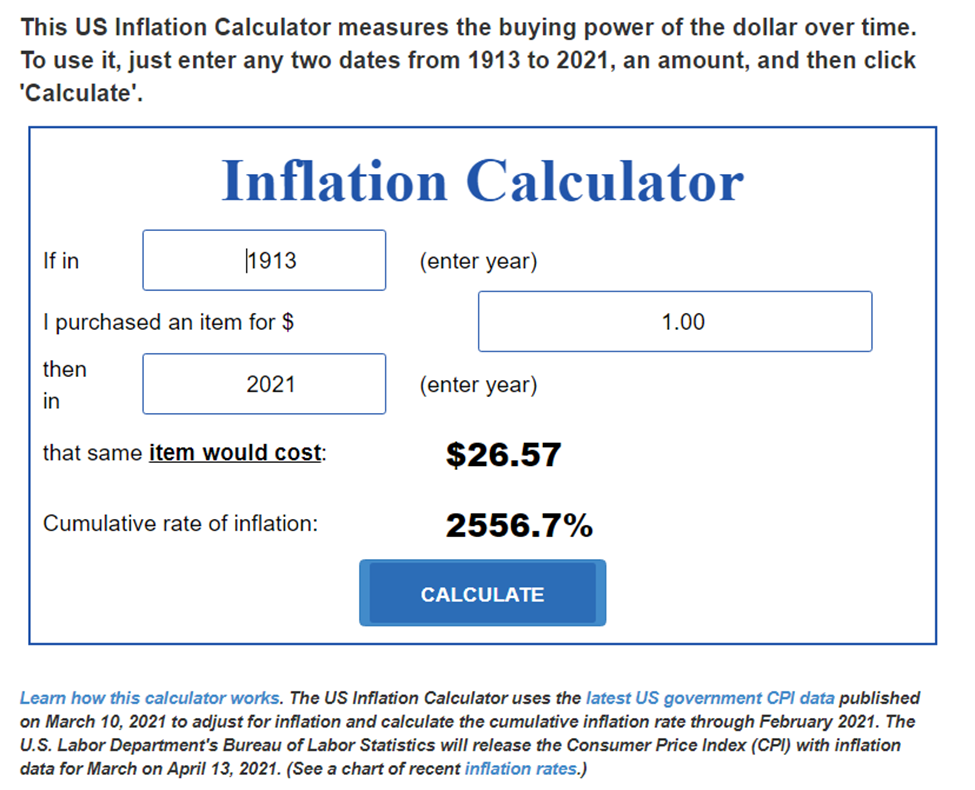

From a different perspective, an item costing $1 in 2013 would cost $26.57 today. A cumulative rate of inflation of 2556.7%

Click Here For US Inflation Calculator

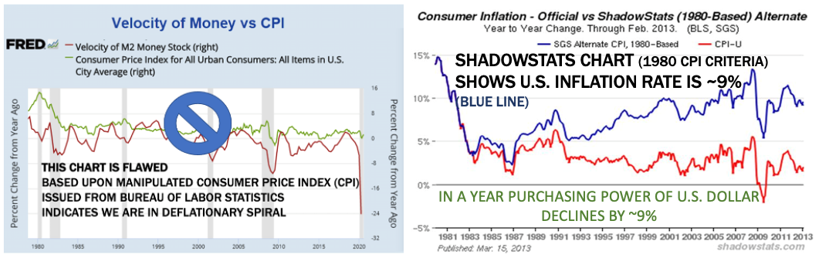

Click Here for Official vs ShadowStats

Do not expect the borrower to refinance as refi applications are now down 72% because most of the people with perfect credit have already refinanced.

No matter what, keep a back door open. What is your exit strategy? Make sure you are covering your “asset “. What if the real estate bubble pops, and property values drop. Now the note investor is facing both eroding buying power  on the monthly payments and a depreciated equity position. If you plan on holding it forever, you are setting yourself up for a loss. Things change. There are Black Swan Events.

on the monthly payments and a depreciated equity position. If you plan on holding it forever, you are setting yourself up for a loss. Things change. There are Black Swan Events.

In essence it means buying any asset class with the end in mind.

Oh, but you say that could never happen? Really.

Ever heard of ENRON. It was flying high in October, 2000. 14 months later, it filed for Chapter 11. Ever heard of Lehman Brothers? It was founded in 1847 and filed for Bankruptcy in September, 2008. Too big to fail. Yea, right.

I have personally experienced the pain of 3 huge cycles. 1981, 1991, and 2008. I am speaking totally from experience. I was a legend in my own mind. When the bubble pops, expect a lot of pain or set yourself up to thrive.

So, let’s distill it down to basics when buying notes.

What does this mean for you the seasoned or newbie note investor? What should you do?

Phrased another way is all about WHEN TO BUY AND WHEN TO SELL.

Prepare for the unknown before you pull the trigger. Investing is a risk. Plan for the worst, and hope for the best.

Remember profits/yield is not realized until you sell. Do not get drunk chasing yield. Focus on return of capital vs return on capital. Think about how to get out, if a worst case scenario pops up. My recommendations have NOT changed since 2015 when I organized the Phoenix Note Investors Forum.

The following recommendations are very simple and straight forward:

#1. Recommendation–Get back to basics.

#2. Recommendation—Get Back to Basics

#3. Recommendation—Mitigate the inevitable.

#4. Build in your stop losses.

The real estate industry has been propped up by the FEDS for a while.

This reminds me the story of the old turkey farmer and how he encouraged his new poults to grow. For 100 days he come into the turkey yard playing music and spreading out handfuls of grain. Eventually the now growing poults became totally friendly toward him. They relied on the goodies. Then on the 100th day he came into the yard—carrying a manchette. They had no clue what hit them. They were so set up.

Does this resonate? I am not sure about you but I’d rather be the farmer vs the turkey on the 100th day.

Why not plan on being the farmer? Today, the economy is/has been propped up with fake everything. Investors are on a drunken high. No clue of what is going on. Another black swan event couldn’t happen again. Could it?

With that in mind let’s go back to my current filters when buying notes to mitigate risk. When buying performing notes, don’t get drunk on yield. Take several factors in mind. When figuring out the LTV, take the current BPO value, subtract 20% and then take 60% of that # to filter LTV for future what if scenarios. Let’s put that in perspective. Asset values can, will and do drop. As they drop, your investment is more exposed to what if situations. But, as the upb decreases, your investment becomes safer.

Assume a BPO value of $100,000 x 80% = $80,000 x .6 = $48,000 for LTV purposes. Factor in $40 monthly servicing fees to calculate your current yield. Servicing fees are INCREASING. Shops that were charging $30 are in some cases charging $40/month. Some less.

Look at the pay history of the borrower. Is it solid? What do they do for work? If they work at a restaurant or other industry hit hard in COVID, evaluate your risk. What happens if they loose their income? Do you want to own the Asset if they stop paying? Cover your back side for what if situations.

There are no rules in today’s market place. There is no rhyme or reason. Remember the lawmakers can change anything at any time. If eviction rules can be changed with the stroke of a pen, so can foreclosure laws. What happens if you buy an NPN and you cannot foreclose? What happens if a perfectly reliable, great paying borrower stops paying due to a Black Swan Event? You are left to work it out—receiving proceeds that are not worth what they are today. When the NPN volume increases in the next 12 months, keep your filters in place. In 2014, I was buying NPN assets with an ITV and LTV not exceeding 30-35% depending on the asset. Allow for the unknows. NPNs can be messy. Taxes, title and blight will take you to the turkey yard. I was conservative. It worked well.

At this time, I am only buying short term performing notes at a steep discount. That is a way to keep the value of your investment in check. Your risk will be reduced every time a payment is made. When the market drops/stalls and it will, you are where you are. There is no going back. Be prepared for the pain and jump the opportunities.

To learn more on the strategies I employed in the year of COVID 2020, go to the Cash Flow Expo 2021 video series @ https://bit.ly/3voMEkY Buy the video series.

Survive and thrive when this economic crash comes. Be the hunter vs the hunted.

When one typically is buying it is about greed. When one is selling it may very well be about fear.

When they intersect, there could be challenges.

Bottom line it is all about When To buy and When To Sell.

NOTES AS WELL AS MOST ASSET CLASSES ARE OVERVALUED.

The dollar is loosing value, therefore your payments in 3+ years will not buy as much. Your unpaid principle balance will not worth what it is now. You have become the turkey vs the farmer. Situs slot gacor.

Set yourself up for success in the years to come.

Avoid being slaughtered.

To learn more about what due diligence strategies when buying which will set you up for a profitable sale go to the Capstone Capital Utube series @ https://bit.ly/31hrvuW

Feel free to call me @ 480 232 5477 or email me at Dave@CapstoneCapitalUSA.com

Wish you all the very best!

|

Recently I was interviewed by Kevin Shortle about a note purchased in 2016. It is a great crystal ball into what is on the horizon with the thousands of non-performing loans in Q for the near future, most likely in early to mid 2021.

This case study will give you a great view into what can happen when a deal goes bad and you know how to handle it.

Visit My Page : TOYIBSLOT

Recently I had the honor of being interviewed by Tom Olson of Good Success

Visit My Page : TOYIBSLOT

Let us clear something up regarding the last financial crisis with housing at the center of the market unraveling. The vast majority of the foreclosures that happened in the Great Recession occurred on standard 30-year fixed rate mortgages. There is this mythology that only subprime and NINJA (no income, no job, no asset) loans were the culprit of the entire collapse. This narrative fits into the crony capitalist mentality that somehow, only losers caused the crisis and that of course all of the suckers that got lured into a toxic mortgage somehow deserved losing their homes (while banks of course got bailed out with billions of tax payer dollars). A swift kick to the poor, and corporate welfare for the banks. It almost fits into this modern psychology of dis-information and revisionist history that we are now seeing. So it should be no shock to rational individuals that now, we suddenly have a whopping 4.7 million mortgages in forbearance (aka not paying their mortgage payment). This is not a good thing. The assumption is that people are going to start paying their mortgages back on time once the virus goes away but is that the case with so many jobs being lost? First, let us show you some data on the previous crisis for those that somehow forgot who lost their homes based on the type of mortgage on the property.

Visite my page: Toyibslot

In March of 2020 Capstone sent letters to 10 borowers to determine if offered a slight discount, would they be interested and able to pay of their mortage. 3 replied yes. They were thrilled. It was a win for the home owner–to own their home outright. It was a win for Capstone to recapture capital to redeploy for other opportunities. Kevin Shortle and I discuss this in the following short video

Visit my page: TOYIBSLOT

Capstone recently purchased several low balance Contract for Deeds and sold 3 small partials which were tagged “Partials For Beginners”. They were sold before all of the COVID-19 mess. This is a situation that evolved truly by accident. The variables were such a new investor could make that big decision to “jump in” and buy their first note without any real risk. Even with the uncertainities of COVID, the investors funds are relatively safe.

One may ask, “Why minimal Risk?”

They all had great basic analytics. Meaning, low Investment to Value(ITV)< 35% & low Loan to Value(LTV) <50%. All the loans had a great pay history–greater than 5 years with real negatives. The payors insurance was in place. They were professionally serviced. They all had a low investment entry point of less of than $11,500 and a partial amortization schedule of <46 months.

Normally a partial is only viable with a larger # of payments remaining –typically over a 100. In this case, the partials were viable due to the superior buying power of Capstone resulting in a winning combination for the partial buyer and Capstone.

I asked each investor why they chose to buy. To the person, it was the set up.

Meaning:

Check out this short utube detailing the deal points and similiarities of each transaction.

Visit my page: Toyibslot

Special Guest Speaker: Howard Tenn

Topic:

Risk vs Reward | Greed vs Fear

Prepare yourself for the next BIG Correction.

What happens when the music stops?

Being a former financial planner, Howard understands this topic.

Lunch served.

Click on the link below to reserve your spot.

$16.83 includes networking, education, lunch, tax and tip.

$20 at the door.

{kind=link}

{kind=link}