https://www.youtube.com/watch?v=Q68tqYQiu2g

Real Estate Note Buyers and Seller Carry Consultants

Editors Note: The following was written by Michael Maharrey and appeared in shiffgold.com.

While is is written by the Gold expert Peter Schiff, the principles, the overlay is expressed as to what is really going on in peoples thought processes.

Bottom line change is in the wind. JPMorgan Chase boss Jamie Dimon urged investors Wednesday to prepare themselves for turbulence in the market in the weeks ahead – warning that extraordinary financial circumstances were creating a potential “hurricane” for the economy.

“It’s a hurricane. Right now, it’s kind of sunny, things are doing fine, everyone thinks the Fed can handle this,” Dimon said during a conference sponsored by AllianceBernstein, according to Bloomberg.

“That hurricane is right out there, down the road, coming our way,” he added. “We just don’t know if it’s a minor one or Superstorm Sandy or Andrew or something like that. You better brace yourself.”

We cannot hide from what is coming. My question to you is, ” Do you have the financial resources if your note payor stops paying? What is your backup plan? Capstone Capital USA has the resources to provide you a lump settlement for all or for a portion of your seller financed mortgage. We will provide a fair market FREE quotation.

Doesn’t it make sense to be proactive while the payor is still current with their payments vs being late causing you to market a note with a developing  poor pay history? Read on…I believe you may identify with the following narrative……….

poor pay history? Read on…I believe you may identify with the following narrative……….

_________________________

Average people are worried about the economy. Consumer confidence has been falling. People undoubtedly feel the squeeze of inflation. But despite their general discontent, most people don’t seem to think a severe economic downturn is imminent — despite many warning signs.

Why not?

Peter Schiff has been warning that a recession is in all likelihood already here. In a recent interview on NTD News, he emphasized that the economic downturn will be much deeper than anybody expects.

I don’t think it’s going to be a mild recession. I think this recession is going to be worse than the Great Recession that started following the 2008 financial crisis.”

But most people remain sanguine about the economy. They may fret a bit about ongoing inflation – as reflected in the consumer sentiment numbers – but they assume the Fed will be able to tame the inflation dragon with some modest monetary tightening. They even concede this might cause a minor recession, but the mainstream believes Jerome Powell when he claims the economy is strong enough to handle higher interest rates and some balance sheet reduction. Virtually nobody besides Schiff and a few other contrarians sees anything major economic problems coming down the pike.

But as Schiff pointed out in that same interview, nobody saw the 2008 recession coming either.

In fact, when we were six or seven months into that recession, the Federal Reserve and other economists still claimed that there was no recession anywhere in sight. So, this recession is going to be much worse than that one.”

In retrospect, the signs of a housing crash were pretty obvious in 2006 and early 2007. It was apparent that there were serious problems in early ’08. But almost nobody in the mainstream saw the financial crisis and Great Recession coming. Like today, there were only a few voices in the wilderness sounding a warning.

Why is it that so few people are prepared for economic crashes when the warning signs are so obvious?

There are certainly many factors, but one likely reason people don’t can’t see the train hurtling down the tracks is a psychological phenomenon known as “normalcy bias.”

In a nutshell, normalcy bias is a form of denial based on the assumption that everything will continue as normal. Bocoran pola gacor hari ini.

Here’s a more formal definition.

Normalcy bias is a psychological state of denial people enter in the event of a disaster, as a result of which they underestimate the possibility of the disaster actually happening, and its effects on their life and property. Their denial is based on the assumption that if the disaster has not occurred until now, it will never occur.”

In simple terms, it’s the “it can’t happen to me (or us)” syndrome.

Normalcy bias leads to inaction. It’s one of the reasons people often ignore hurricane warnings. The assumption is “we haven’t ever had a hurricane yet, and if we do, it probably won’t be that bad.”

According to PsycholoGenie, there may be some evolutionary basis for normalcy bias.

There is a theory that associates normalcy bias with the evolutionary aspect, that suggests that paralysis gives an animal a better chance of survival because predators are less likely to attack and feed on something that isn’t moving.”

That’s great if predators are hunting you in the jungle. It’s not so great if an economic disaster is looming.

I think normalcy bias is one of the reasons the Federal Reserve’s transitory inflation narrative gained so much traction. Despite the money printing after the 2008 financial crisis, consumer prices never rose as many predicted. Instead, inflation manifested in asset prices, particularly stocks and real estate. This led Fed policymakers to assume they could do quantitative easing again – and even double down on it – without severely impacting consumer prices. Of course, the dynamics were different during the pandemic. Not only was the Federal Reserve printing trillions of dollars, but the US government was also handing out cash in the form of stimulus checks, even as most Americans were sitting at home producing nothing. This was a recipe for rapidly rising consumer prices.

But normalcy bias kicked in. We were told, “Inflation didn’t happen before, so don’t worry, it won’t happen now.” An assumption set in – things will continue as they always have. And when prices started to spike, these same people assured us that it was transitory. All along, Schiff was warning that inflation wasn’t transitory. But pretty much nobody listened.

Similarly, I think normalcy bias has played a role in gold and silver’s lackluster performance in recent months. As Schiff put it in a video on the recent performance of gold, “Even though we have a lot of inflation today, investors still think we won’t have inflation tomorrow.”

Because the Fed has been able to raise interest rates to keep inflation at bay in the past, the mainstream just assumes it will be able to modestly raise rates and keep inflation at bay this time around. Never mind that there are different dynamics in play and plenty of signs that inflation will likely remain entrenched over the coming months. Normalcy bias has blinded people to the fact that it would require a Paul Volker style hike to push real interest rates into positive territory — the only cure for inflation.

At some point, reality will cut through the normalcy bias. It always does. But when the mainstream wakes up, it’s too late.

As you survey the economic landscape, be aware of normalcy bias. There is no reason to assume things will continue as they always have. Keep your eyes on the economic data, analyze it objectively and keep basic economic principles in mind. And then, prepare accordingly.

Fannie Mae has approved attorney foredclosure fees. One of the first questions that is asked regarding any real estate foreclosue is “What does it cost”? This  topic was discussed at the February 2020 NoteWorthy Summit. Some Attorneys charge by the hour. Some attorneys charge by Fannie Mae allowable limits. My experience is do NOT hire an attorney by the hour. The attached list details allowable costs by state. But………….keep in mind there are other costs. Ask your attorney for those details so you know your options. For instance, one of the more expensive counties for foreclosure is Allegany County(Pittsburg). The Sheriff charges $2,500. Yikes!!

topic was discussed at the February 2020 NoteWorthy Summit. Some Attorneys charge by the hour. Some attorneys charge by Fannie Mae allowable limits. My experience is do NOT hire an attorney by the hour. The attached list details allowable costs by state. But………….keep in mind there are other costs. Ask your attorney for those details so you know your options. For instance, one of the more expensive counties for foreclosure is Allegany County(Pittsburg). The Sheriff charges $2,500. Yikes!!

The costs are different for Land Contracts/Contract For Deeds. That may be a different process which is referred to as forfeiture. Some states now view Land Contracts/Contract For Deeds just like a foreclosure. Some states have a relatively short process(Texas-60 days). Other, Florida, New York, New Jersey may take 2+ years to foreclose. Typically the “sand” states have a short fuse–Arizona, California etc. As an investor, Capstone avoids the states North of and including, Maryland/New Jersey due to the anti-investor seniment. Be smart, check out the laws first before you invest. If you own a real estate note, or contract, performing or non-performing, Capstone Capital USA buys notes and mortgages. Give us a call.

Fannie Mae_allowable-attorney-trustee-foreclosure-fees

Special Guest Speaker: Howard Tenn

Topic:

Risk vs Reward | Greed vs Fear

Prepare yourself for the next BIG Correction.

What happens when the music stops?

Being a former financial planner, Howard understands this topic.

SAVE THE DATE.

MARK YOUR CALENDAR

YOU WANT TO BE IN ATTENDANCE!!!

FOR WEDNESDAY FEBRUARY 5th

NOTE INVESTORS FORUM

Lunch served.

Click on the link below to reserve your spot.

$16.83 includes networking, education, lunch, tax and tip.

$20 at the door.

Several years ago–going way back to the late 1990’s I had the pleasure of meeting and working with  Jeffery Combs of Golden Mastermind Seminars in a large MLM venture. Subsequently, Jeffery went on to build a huge personal development business. Prior to meeting Jeff, I had a fair amount of sales training via Dale Carnegie and the AMWAY business.

Jeffery Combs of Golden Mastermind Seminars in a large MLM venture. Subsequently, Jeffery went on to build a huge personal development business. Prior to meeting Jeff, I had a fair amount of sales training via Dale Carnegie and the AMWAY business.

So what’s this post about? Bottom line —working with people and watching their body language. If you work with or interact people the year 2020 is no different than 1990 or 1998. This post is about integrating people skills into what ever business you are in. Notes, investing, real estate or whatever. It even works in personal realtionships!!! Technology is great, but people skilss is where the rubber really meets the road.

The full article is below, but you can also click on the picture to access the article and Jeffery’s site.

Personally I Read Body Language @ the Note Investors Forum Meetup and every time I speak on stage or even on the phone–which is can be done by listening very carefully to voice inflections.

____________________________________________

Connecting with people is easy.

You shake their hand, say hello, and ask genuine questions to get to know them.

But do you know what the person is saying beyond their words?

Let’s face it…

…If you can’t read between the lines of what they are saying or aren’t paying attention to their body language… you are missing the boat!

I know…

I’ve been in sales for over 35 years and have been a success and addiction coach for 20 years PLUS!

It’s critical that you understand how to read energy, body language, non-verbal communication, what is meant along with what’s said, and be able to read why people do what they do.

Why… you ask?

Because body language and non-verbal communication can account for over 60% of what is being communicated.

So today, I’m going to teach you how to read the signs.

A frown means someone is sad or disappointed.

An upturned mouth means a person is happy. You learned this at a very young age without anyone formally teaching you.

Over time, you began interpreting expressions and body language.

Here’s what you require knowing today…

Human beings are predictable. The more you understand people’s predictability, the better you will be it be able to adapt and adjust to the situation.

NOW, to be in an emotional space to read people on a deeper level, you have to get beyond the fear of judging people. Being able to read people effectively DOES NOT mean you’re judging them.

It means that you live in a know state… That’s K-N-O-W. Not N-O. Meaning you see the signs, interpret them, and KNOW what is communicated.

Have you ever seen someone who broods and pouts? Their bottom lip comes up over their top lip. Then their energy drops.

Have you ever encountered someone who’s hostile and unapproachable and you could tell how angry he or she was without talking to him or her?

These are just a few examples of non-verbal communication that you require interpreting to understand body language.

So here’s the thing…

The psychology of reading body language is not that difficult once you become aware of the signs.

Watch the person’s eyes.

When you ask someone a question… a simple a yes-no question like, “Have you ever considered starting your own business?” And the person answers with the sound, “Um” followed by a “Well…”

Realize these are stalling words. They are a CLUE you know you’re going to receive a story.

Pay attention to words of indecision like guess, kind of, and sorta. These are words of non-commitment.

When you ask someone a question, and they cross their legs or cross their arms… This is a clue that they are shut off or overwhelmed.

If the person has very little or a tense facial expression, their body is turned away from you, or their eyes are downcast, maintaining little contact… this typically means they are disengaged, not interested, or unhappy.

On the other hand, when you ask a person a question, and they respond immediately, this is a positive sign.

Here’s a bigger clue…

If they use a superlative like: Yes, Absolutely, or Unequivocally… this is a sign that the person is decisive. They are someone who can commit.

Examples of positive body language signs include: having an open body position… that means the arms are unfolded and hand gestures will face up. The person will hold an upright posture and have a relaxed facial expression. There will be regular eye contact… And the person’s arms will be relaxed by their sides when they are not gesturing.

O.K.

Here is one of the biggest secrets when it comes to reading the signs.

As you observe the body language of a person, also PAY ATTENTION to what’s meant… not what’s said.

What does that mean?

You can intuitively know what they mean by what they say.

I’ve been a sales professional for 35 plus years. Often, people tell me what they think I want to hear.

Here are some examples:

“Yeah, what I’m going to do is look over this information, and I’m going to get back with you.”

“Yeah what I’m going to do is hire you just as soon as I get my money together.”

“Um… I’ll call you after the holiday.”

“This sounds great BUT… I have to run it by my spouse.”

It’s your responsibility to understand who means what they say and who’s telling you what they think you want to hear.

When someone says to me, “I’m sure you can appreciate I have to run to buy my husband.” In reality, I appreciate someone who can make a decision. The person is assuming that I’m going to agree with them.

Now, I’m not going to disagree with them, but I understand what that means. I also know that some people DO require to speak with a significant other. I do understand that they require to get approval from someone else or acknowledgment.

BUT I also ask a question to test the situation.

“Can you close your husband?”

“Can you close your significant other?”

“Are you going to be able to ask for a loan from your bank?”

These are situations where you learn to ask further questions.

When you get good at reading people, you can see the non-verbal communication in their eye irises. You can see it in the smirks in their face. You can see the downtrodden corners of their mouth. You can see how high or low their energy is.

And by interpreting the tone of a person’s voice, you can hear vibrationally where he or she is coming from.

Be attentive when you ask a question.

Does the person cross his or her legs? Do they look away? Does his or her eye iris’s go up and out? Does the sound “UM” come out of his or her mouth? Does the person start telling you a story completely unrelated to the question you ask?

Watch the person’s body language. See how closed and contained he or she is…

…or how open he or she is.

These are all telegraphs… They are signs.

The more you pay attention to the signs, practice interpreting the non-verbal communication, and read body language… the better you will become at the science of reading people.

I thought this post by Jim Ingersol was so to the point. Just outstanding. Jim and I met on a Walter Wofford / Quest IRA cruise several years ago. Jim and his wife Janice live in the Richmond, VA area. He is a real pro. Trustworthy and to the point. A no BS type of guy. A great human being!!

Let’s start by looking forward 10 years, to the year 2030. What do you really want your life to look like? Take a minute and write down your answers to the following 5 questions.

1. Who do you want to be spending the most time with?

2. How physically fit do you picture yourself?

3. How much time freedom do you want and what do you want to do with it?

4. Where will you want to travel (and with who)?

5. What impact do you hope to be making in 2030?

All things are possible, but first you have to know where you are heading and then believe in yourself to make it happen. You have to dig deep and really discover your “why.” Without knowing your “why” you will likely run away from your dreams as soon as you hit your first obstacles. So how do you really find your own “why?”

2019 in review – Now take a look back at 2019 by looking through your photos on your phone (and in facebook), look through your dropbox, review your journal, take a look at what went great and what your business struggles were, look through your dropbox and your journal along with the places you went and the people you met in 2019. Which things brought the most joy and what did you learn in your struggles? Reflection can be an important piece of planning for your future!

The two most important days in your life are the day you are born and the day you find out why.

– Mark Twain

CLICK HERE FOR THE FULL ARTICLE

Special Guest Speaker: Stan Harley

Topic:

Economic Predictions – 2020 and beyond

YOU NEED TO SAVE THE DATE.

MARK YOUR CALENDAR

YOU WANT TO BE IN ATTENDANCE!!!

FOR WEDNESDAY JANUARY 8th

NOTE INVESTORS FORUM

Lunch served.

Click on the link below to reserve your spot.

$16.83 includes networking, education, lunch, tax and tip.

$20 at the door.

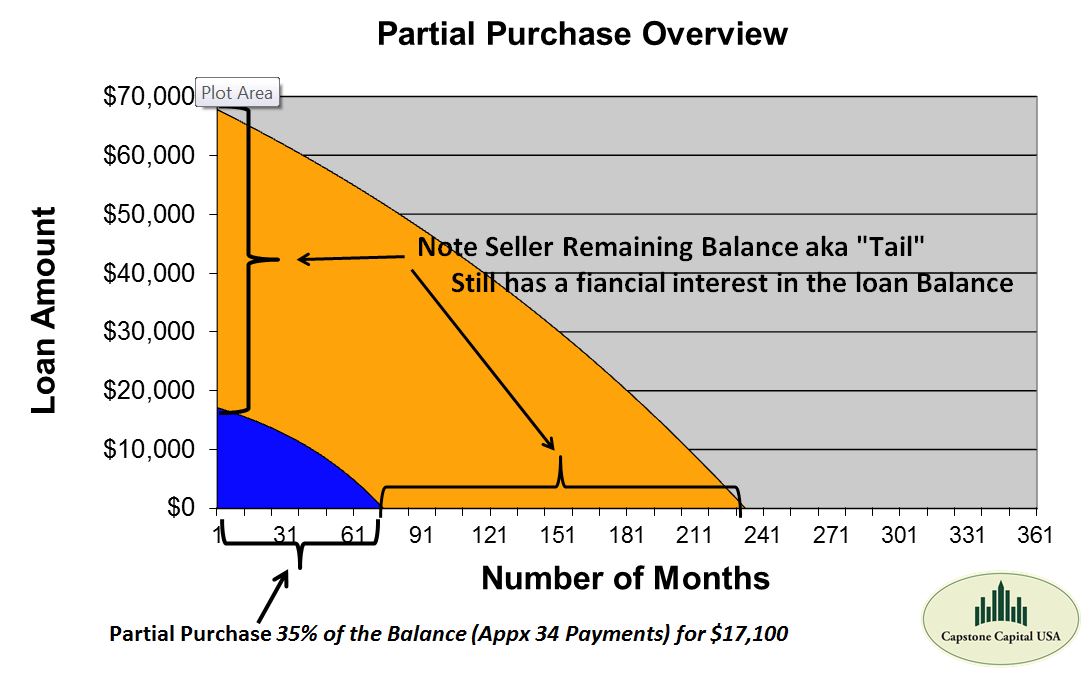

QUICK QUESTION………..

Do you have an interest in buying

INVESTMENT GRADE PARTIALS?

TO BE ADDED TO OUR PREFERRED CONTACT LIST

Capstone only buys and Capstone only sells

Investment Grade Notes.

FIND OUT WHY HERE

For a Deep Dive into Partials

Watch a Short Utube Video Overview

CHECK OUT OUR UTube Channel for Free Education

![]()

When you start the process of selling your mortgage note it’s important to keep in mind that how much a mortgage note sells for mostly comes down to risk. Typically, the less risk involved in the note, the greater its market value.

One of the first things a note-purchasing company looks at is the value of the property that serves as collateral on the note. The current market value of the residential or commercial real estate listed on the note can increase or decrease the note’s market value.

Keep in mind, the amount listed on the mortgage typically is not the same thing as the current value on the property, or the amount for which the property was last purchased. Real estate values can fluctuate over time. If you’re not sure of the current value of your property, online resources such as Zillow can provide a rough estimate. During the note-selling process, a more precise quote is given.

A factor which affects property value is the actual type of the property. Typically single family dwellings maintain higher values than other property types like condos or manufactured homes.

The equity the real estate’s owner has in the property factors into the value of the note. This includes the amount of the down payment, as well as payments already received from the property owner.

When a payer has invested a significant portion of his or her own assets into the real estate, the payer has a vested interest in the real estate and is less likely to default on the loan. Thus, a mortgage note with a significant level of equity from the buyer presents a lower risk.

The more equity the homeowner has, the more money a note seller is typically able to get for the note.

The mortgage note owner’s creditworthiness does not factor into the sale of the note, but the property owner’s creditworthiness does.

The higher the credit score of the property owner, the higher the value of the note. More creditworthiness in the owner means the person purchasing the payments is taking on less risk. Because the buyer of the note is assuming less risk, that money is passed on to the seller.

A low credit score does not automatically mean the note can’t be sold. Other factors such as payment history on the note, and the payer’s equity in the property, can help in cases where a low credit score hurts. Still, a lower score means more risk and thus degrades the note’s value.

Payment history on the note also determines how much a mortgage note is worth. This concept is often described as notes either being “performing,” meaning having regular payments, or “non-performing,” which means the payments have not been paid on time.

Being able to show a strong payment history from the property owner can make your mortgage note more valuable.Most private mortgages are not reported to credit bureaus, and so the payments do not influence the payer’s credit score. Thus, positive credit history on the mortgage note can help compensate for a payor having a weaker credit score.

If the payer on the private mortgage is a corporate entity, trust or nonprofit, it helps to have an individual listed as the personal guarantee of the payer. By having a guarantee, it means the note has recourse in the event the entity, trust or nonprofit stops making payments on the loan.

The term “recourse” means the note has someone with whom recourse could be taken in the event the loan is defaulted upon. Though it does not bar it from being saleable, a nonrecourse note has significantly more risk, which degrades its value.

Interest rate and the length of a loan also help determine the value of the note. A higher interest rate and shorter loan term make for a more valuable note.

Other note terms, such as a rider on the mortgage affecting the term, can also affect its value. For instance, some private mortgage notes have a balloon rider. This type of rider lets smaller payments be made for a time, with one lump sum due at the end of the term. This would be instead of evenly distributing the amount due over a series of payments. Any rider affecting the payment schedule can affect the value of the note.