Selling your mortgage note is not all about or just about price. It is also about working wit a buyer who will follow through and actually close at the agreed price. If you have a note to sell and you are not sure who to call, who to trust or what to look for yo will want to watch this short 9 minute video

What’s My Note Worth?

What’s My Note Worth?

A question all note sellers have and have a right to know.

Timing Your Mortgage Note Sale is everything.

So, when is the correct time to sell your mortgage note?

REAL ESTATE PRIVACY–PROTECT YOUR ASSETS

The following utube video with my friends Walter Wofford and Jim Ingersoll is so to the point as to the value of trusts in any form of a real estate transaction.

They discuss the ultra importance of transactional privacy and how that helps with asset protection.Under what circumstances would you want the general public to know the properties you own?

Trusts provide privacy and effectively separate all of your investment assets. They are not hard to use and provide tremendous privacy in your deals as a trustee is used to hold title and the trust agreement is not recorded at the courthouse.

Under what circumstances would you not like the public to know that you own a property?

What are the benefits of using trusts?

1. Privacy – Keep your name and LLC out of public records

2. Liens and judgments

3. Probate benefits

4. Sell the entity, not the property

5. Personal property trusts for IRAs, cars, boats, etc

Borrowing our way out of Debt

Today I cam across this article title,” The Three Ds of Doom: Debt, Default, Depression”. Without sounding negative, it certainly makes one think about the current economy. Everything appears to be booming, at least here in the greater Phoenix Metroplex. But………..what is under the covers. What goes up always comes down. It is a fact of life. Now apply this to the niche business. It is the paper side of real estate.

In the very near future, Capstone will be launching a Utube note training series on buying Notes. One of the topics as part of the due diligence series will be a deep dive into Investment to Value and Loan to Value. In other words, what is the note buyers safety net in the event of a downturn. How to minimize the pain in your portfolio. The only way I know is to have an EQUITY SPREAD. For instance, if a note has a $100,000 unpaid loan balance (aka UPB), what is your risk tolerance. What safety net do you require? The Capstone safety net is an Investment to Value (ITV) not exceeding 65% and a Loan to Value not exceeding 70%. Some say this is too big a filter. I guess time will tell. Anyway–moving on to the article.

The Three Ds of Doom: Debt, Default, Depression

July 17, 2019

“Borrowing our way out of debt” generates the three Ds of Doom: debt leads to default which ushers in Depression.

Let’s start by defining Economic Depression: a Depression is a Recession that isn’t fixed by conventional fiscal and monetary stimulus. In other words, when a recession drags on despite massive fiscal and monetary stimulus being thrown into the economy, then the stimulus-resistant stagnation is called a Depression. Read more

AUGUST PHX NOTE INVESTORS FORUM MEETUP

![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

The Next Note Investors Forum Meeting will be

Wednesday, August 7th 11:30am-1:30pm

La Famiglia Restaurant, SE corner of Dobson & Guadalupe, Mesa

Case-Shiller: National House Price Index increased 3.7% year-over-year in March

Case-Shiller: National House Price Index increased 3.7% year-over-year in March

S&P/Case-Shiller released the monthly Home Price Indices for March (“March” is a 3 month average of January, February and March prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: S&P CoreLogic Case-Shiller Index Shows Annual Home Price Gains Continue to Weaken

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.7% annual gain in March, down from 3.9% in the previous month. The 10-City Composite annual increase came in at 2.3%, down from 2.5% in the previous month. The 20-City Composite posted a 2.7% year-over-year gain, down from 3.0% in the previous month.

Las Vegas, Phoenix and Tampa reported the highest year-over-year gains among the 20 cities. In March, Las Vegas led the way with an 8.2% year-over-year price increase, followed by Phoenix with a 6.1% increase, and Tampa with a 5.3% increase. Four of the 20 cities reported greater price increases in the year ending March 2019 versus the year ending February 2019.

(NOTE: The Phoenix Market did a complete u-turn NORTH. 45% of all inventory was sold in April. What was a down turn, is now back on track. The Phoenix area is growing by 86,000 people every year. Maricopa County is the fasted growing county in country. CLICK HERE FOR THE LOCAL REIA STATS

New to Market – New Performing Notes

Property Locations

IL IN MI OH TN

BPO Range: $33,000 – $70,000

UPB RANGE: $17,785 – $34,860

PURCHASE PRICE RANGE: $19,000 – $26,200

PRICING RANGE: 76% to 90% of UPB

Re-Performing Loans & Seasoned Performing Loans

Click Here to Access

Case Studies ~ Buy A Performing Note – Then It Goes South — Part 3

CASE STUDY 3

This post is a 3rd in a series of 4 regarding how a perfectly good performing note goes south due to life event situation.

This particular note was in the small town of Marshall, IN. The note -Contract for Deed- was originated in 2009. The payors significant other passed in 2010. My IRA purchased the note in 2015. The note was scheduled to mature in June, 2019. I was unaware of the loss of the male payor. The payment history evolved into a rolling 120 days, meaning after 4 months the payor paid the balance or part of the balance to stay out of the forfeiture procedure. However this payment history caught up with the payor in that there was a $5,000 unpaid balance balloon that went beyond the due date of the note.

Fast forward to February, 2019, I was tired of constantly contacting the payor. I did not want to go thru the forfeiture process as to take back the house –due to condition, was not a viable option. Plus 9 months and $3,000 in attorney fees were not viable. In prior conversations, it was discovered she was the caregiver of her mother and was not working. He current husband was not working. After multiple conversations, she realized she needed help. Her Dad was brought into the conversation. He agreed to help her out. They agreed to bring the payments current. In exchange to removing the deceased payors name from the CFD, they agreed to a loan modification which extended the term 12 months, and stay current. If they ran late past 15 days, the newly executed Quit Claim deed would be recorded and my IRA would own the house.

It was a win-win. The payor benefited by having the deceased partner removed from any claim of ownership, the loan was brought current, I avoided the possibility of a 9 month forefeiture procedure and the payor will own her house free and clear in 12 months with the extension of the balloon due date.

Even though the remaining balance was small, the solution was perfect for all.

I have learned, if one works with the payor and developes a dialog, future unfortunate events can be worked out much easier. But, it is all about how can the payor feels and appreciates that they are being helped so they will be open to a solution which also benefits the note holder in the event needed.

This case study was presented at the May 1 Note Investors Forum Meetup

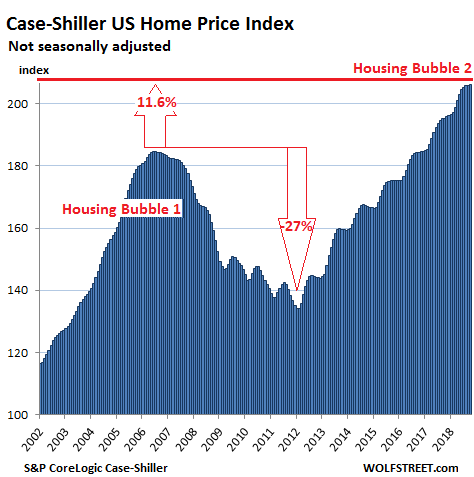

The Most Splendid Housing Bubbles in America

I found this article backed by statistics. While each market is local, there are some trends when looked at as a whole. Phoenix may not be far behind. A slowing market will require motivated sellers to consider seller financed transactions vs just cash. For those in the note business, this creates wonderful opportunities.

The Most Splendid Housing Bubbles in America Decline

by Wolf Richter • •

Seattle house prices drop 4.4% in four months, biggest drop since Housing Bust 1; Prices deflate in San Francisco Bay Area, San Diego, Denver, and Portland.

Some of the markets in this select group of the most spending housing bubbles in America have turned the corner, according to the S&P CoreLogic Case-Shiller Home Price Index, released this morning for October, confirming other more immediate data. This includes the Seattle metro, the five-county San Francisco Bay Area, the San Diego metro, the Denver metro, and the Portland metro. In these metros, house prices have skidded the fastest, and in some cases for the first time, since the Housing Bust. In other markets, house prices have been flat for months. And in a few markets on this list, prices rose. More on those markets in a moment.

On a national basis, these dynamics get washed out. Single-family house prices in the US, according to the S&P CoreLogic Case-Shiller National Home Price Index, ticked up a smidgen on a month-to-month basis in October, and rose 5.5% compared to a year ago (not seasonally-adjusted). This year-over-year growth rate has been slowing from the 6%-plus range that reigned from September last year to July this year. The index is now 11.6% above the July 2006 peak of “Housing Bubble 1” (the first housing bubble in this millennium), which came to be called “bubble” and “unsustainable” only after it had begun to implode during “Housing Bust 1”:

The index is a measure of inflation — not of consumer price inflation but of house-price inflation, where the same house requires more dollars over the years to be purchased. In other words, the index shows to what extent the dollar is losing purchasing power with regards to buying the same house over time.

The index is a measure of inflation — not of consumer price inflation but of house-price inflation, where the same house requires more dollars over the years to be purchased. In other words, the index shows to what extent the dollar is losing purchasing power with regards to buying the same house over time.

The Case-Shiller Home Price Index is a rolling three-month average; today’s release is for August, September, and October data. Based on “sales pairs,” it compares the sales price of a house in the current month to the prior transaction of the same house years earlier. The index incorporates other factors and formulas to arrive at each data point.

Is The Phoenix Housing Market on Borrowed Time?

The next Phoenix Note Investors Forum will be

Wednesday January 9th, 2019

Guest Speaker – Stan Harley ![]()

MEETING TOPICS —Economic Predictions 2019

Is The Phoenix Housing Market on Borrowed Time?

RESERVE YOUR SPOT ON THIS SITE

Attendance capped at 55

Full buffet lunch.