![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

Real Estate Note Buyers and Seller Carry Consultants

![]()

The August 7th Note Investors Forum Meetup focus on:

TOPICS: Several New Case Studies

Where Does a New Note Investor Begin

Bring your questions, This will be an interactive meeting.

![]()

S&P/Case-Shiller released the monthly Home Price Indices for March (“March” is a 3 month average of January, February and March prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: S&P CoreLogic Case-Shiller Index Shows Annual Home Price Gains Continue to Weaken

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.7% annual gain in March, down from 3.9% in the previous month. The 10-City Composite annual increase came in at 2.3%, down from 2.5% in the previous month. The 20-City Composite posted a 2.7% year-over-year gain, down from 3.0% in the previous month.

Las Vegas, Phoenix and Tampa reported the highest year-over-year gains among the 20 cities. In March, Las Vegas led the way with an 8.2% year-over-year price increase, followed by Phoenix with a 6.1% increase, and Tampa with a 5.3% increase. Four of the 20 cities reported greater price increases in the year ending March 2019 versus the year ending February 2019.

(NOTE: The Phoenix Market did a complete u-turn NORTH. 45% of all inventory was sold in April. What was a down turn, is now back on track. The Phoenix area is growing by 86,000 people every year. Maricopa County is the fasted growing county in country. CLICK HERE FOR THE LOCAL REIA STATS

Property Locations

IL IN MI OH TN

BPO Range: $33,000 – $70,000

UPB RANGE: $17,785 – $34,860

PURCHASE PRICE RANGE: $19,000 – $26,200

PRICING RANGE: 76% to 90% of UPB

Re-Performing Loans & Seasoned Performing Loans

Click Here to Access

The following article appeared in DSNEWS.

House prices are rising.

There is a shortage of housing.

There is a shortage of rentals.

There is a shortage of well priced notes & REO’s.

“Prices are growing more quickly in some places than in others, and in MSAs where recovery has been most robust (and even in surrounding metros), price growth is probably not the best metric to use for rental investors seeking a new property to buy and hold.

So………….which MSAs have the best rate of return on rental investments?

The following article was from CNBC.

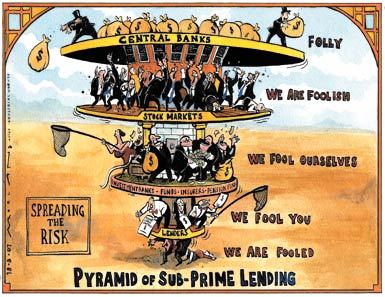

Having lived and felt the pain of the subprime crisis, the return to subprime is a recipe for disaster. No different than the movie The Big Short or the book Fools Gold!!

They were blamed for the biggest financial disaster in a century. Subprime mortgages – home loans to borrowers with sketchy credit who put little to no skin in the game. Following the epic housing crash, they disappeared, due to strong, new regulation, and zero demand from investors who were badly burned. Barely a decade later, they’re coming back with a new name — nonprime — and, so far, some new standards.

California-based Carrington Mortgage Services, a midsized lender, just announced an expansion into the space, offering loans to borrowers, “with less-than-perfect credit.” Carrington will originate and service the loans, but it will also securitize them for sale to investors.

“We believe there is actually a market today in the secondary market for people who want to buy nonprime loans that have been properly underwritten,” said Rick Sharga, executive vice president of Carrington Mortgage Holdings. “We’re not going back to the bad old days of ninja lending, when people with no jobs, no income, and no assets were getting loans.”

Sharga said Carrington will manually underwrite each loan, assessing the individual risks. But it will allow its borrowers to have FICO credit scores as low as 500. The current average for agency-backed mortgages is in the mid-700s. Borrowers can take out loans of up to $1.5 million on single-family homes, townhomes and condominiums. They can also do cash-out refinances, where borrowers tap extra equity in their homes, up to $500,000. Recent credit events, like a foreclosure, bankruptcy or a history of late payments are acceptable.

All loans, however, will not be the same for all borrowers. If a borrower is higher risk, a higher down payment will be required, and the interest rate will likely be higher.

“What we’re talking about is underwriting that goes back to common sense sort of practices. If you have risk, you offset risk somewhere else,” added Sharga, while touting, “We probably are going to have the widest range of products for people with challenging credit in the marketplace.”

Carrington is not alone in the space. Angel Oak began offering and securitizing nonprime mortgages two years ago and has done six nonprime securitizations so far. It recently finalized its biggest securitization yet — $329 million, comprising 905 mortgages with an average amount of about $363,000. Just more than 80 percent of the loans are nonprime.

Investors in Angel Oak’s nonprime securitizations are, “a who’s who of Wall Street,” according to company representatives, citing hedge funds and insurance companies. Angel Oak’s securitizations now total $1.3 billion in mortgage debt.

Angel Oak, along with Caliber Home Loans, have been the main players in the space, securitizing relatively few loans. That is clearly about to change in a big way, as demand is rising.

As a real estate note professional, the buyer of performing and non-performing notes & REO, the following article confirms/addresses what has been shared from many venues.

The nation has a staggering shortage of 7.2 million affordable and available rental homes for extremely low-income (ELI) renter households, reports MFE sister brand Affordable Housing Finance. Deputy editor Donna Kimura examines a new study from the National Low Income Housing Coalition (NLIHC), The Gap: A Shortage of Affordable Homes, which finds that for every 100 of the lowest-income renters, or those earning 30% of their area median income, there are just 35 homes affordable and available to them.

“This leaves over 8 million of the lowest-income people [spending] more than half of their limited income on rent each month, leaving very little for healthy food, for savings, or to cover an unexpected financial emergency,” says Diane Yentel, NLIHC president and CEO. “The report highlights the urgent need for an increased national investment in more homes affordable to the lowest-income people.”

Yental also noted that federal housing programs serve about 5 million low-income households, but the needs of many more families go unmet. Only one out of every four eligible families receives the help they need. As a result of the housing shortage, low-income unassisted households are often severely cost burdened and pay more than half of their limited income on rent.

The severe shortage of rental homes affordable and available to the lowest-income households predates the Great Recession but has worsened in recent years, according to the study. In 2007, 40 affordable and available rental homes existed for every 100 ELI renter households and 67 existed for every 100 renter households with incomes at or below 50% of the area median income (AMI). A small surplus of affordable and available rental homes existed at 80% and 100% of the AMI in 2007. Since then, the supply of affordable and available rental homes (relative to demand) has declined even at these higher-income levels. Renter households at 100% of the AMI, however, still enjoy a surplus nationally and in most markets.

I was recently interviewed by Eddie Speed, the Founder of Note School of which I have been a Mentoring Student since 2013 and Case Study winner at Note Expo 2017.

We discussed how my successful real estate career kept me so busy it crowded out spending time with my family. As a successful Phoenix REO agent between 2008 and 2014, the REO business dominated my life even more as demonstrated in 2010 when I closed 296 houses. By 2012, I realized the industry was changing. The inventory of houses was declining, which meant my potential to make money was declining.

Changing from being a prolific REO agent to note investing gradually changed my life for the better. I can now enjoy my Grandson and not be worried about being constantly accountable to the asset managers.

I went from being a business owner to a portfolio owner. Plus, I can do deals from anywhere. I’m loving every minute of time I get to spend hiking in the mountains around Phoenix –many times with my daughter and grandson.

<iframe width=”560″ height=”315″ src=”https://www.youtube.com/embed/zErH-53vIC8″ frameborder=”0″ allow=”accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture” allowfullscreen></iframe>

This interview focuses on a Partial Note sale completed in September, 2017. My IRA bought the note, then recouped almost all it’s original investment by selling the first 125 payments as a partial to a passive investor, but kept the next 154 payments. This property is near Detroit and my passive investor lives in Hawaii. I completed this deal from my Phoenix office

Best of all, The ROTH IRA’s profit is 100% tax-free!

The 2018 NoteWorthy Investor Summit awarded Dave Franecki of Capstone Capital USA

the Note Investor of the Year Award.

The Conference was held at the Irvine, CA Marriott.

Dave Franecki has been in the Note investor space since 2013 and works in the Performing | Non-Performing| and REO space. Prior to delving into this  niche asset class, Dave was an high producing REO agent in the Phoenix Metroplex selling over 900 houses during the real estate recession.

niche asset class, Dave was an high producing REO agent in the Phoenix Metroplex selling over 900 houses during the real estate recession.

His real estate career began in 1978 in Cincinnati, OH.

MEETING TOPIC: We’ll walk thru the process of taking a non-performing note to an REO and give examples of how the workout is completed. Basically from purchase to the multiple options to maximize significant returns. We’ll show the passive approach and the more aggressive velocity approach for much higher ROI.

If you have an interest in significantly higher returns than Performing notes, you will want to attend Tuesday April 3rd 11:30am – 1:30pm!!

Look Forward to Seeing You!!!

Dave

RESERVE YOUR SPOT @ EVENTBRITE TICKETS

General Admission / Early Bird Discount price of $16.83

available until Noon April 2nd

Price Includes:

*Admission

*NetWorking

*Education

*Buffet Lunch, Tax & Tip

Just want to show up? No Problem!!

Walkins Always Welcome–$20 @ the door, credit card or cash

includes meal, tax, tip

plus

Networking and Note Training

Email Dave with special dietary needs or special menu needs

A troublesome signal just appeared in the housing market and could put taxpayers at risk.

Federal Housing Administration mortgage delinquencies jumped in the fourth quarter for the first time since 2006, the Mortgage Bankers Association reported Wednesday. The FHA insures low down-payment loans and is a favorite among first-time homebuyers.

The seasonally adjusted FHA delinquency rate increased to 9.02 percent in the fourth quarter from 8.3 percent in the third quarter, MBA data show. The jump, which followed the lowest delinquency rate since 1997, was driven by loans made since 2014 and early-stage delinquencies, those just 30 days past due.

It’s too soon to know if it is a blip or a trend, but the jolt is clearly a warning.

“We had been experiencing great credit quality for so long, and to suddenly see this quarter-over-quarter reversal was a surprise, and we’re looking closely at it,” MBA CEO David Stevens said.

Now, the Trump administration will have to weigh the risks to the FHA portfolio against the weakening affordability in the housing market overall. Young, first-time buyers have largely been sidelined in the housing recovery, burdened by higher costs, tight credit and high levels of student debt. Home ownership is sitting at the lowest rate in 50 years.

“When we see a blip like this, we get concerned about whether that it is a trend,” Stevens said. “And getting these premiums priced appropriately to provide access to home ownership — but also to protect the taxpayer — is that really important balance that the incoming secretary is going to have to focus on with his team to make sure we don’t put the taxpayer at risk or the program at risk — and that’s the challenge.”

Barely a few hours after the inauguration, the Trump administration froze a move by the outgoing Obama administration that would have saved some lower-income borrowers money. It was a cut in the annual mortgage insurance premium on government-insured FHA loans.

The outgoing secretary of Housing and Urban Development announced plans to trim the cost just weeks before President Donald Trump took his oath. The move would have saved the average borrower about $500 a year and could have helped thousands more first-time and lower-income buyers purchase homes. The sudden freeze drew sharp criticism from Realtors and homebuilders who claimed it was overly cautious and burdensome.

The Trump administration defended the freeze in the FHA premium cut, saying only that, “more analysis and research are deemed necessary to assess future adjustments.” That came in a letter signed by General Deputy Assistant Secretary for Housing Genger Charles. HUD Secretary nominee Ben Carson, who has still not been confirmed, addressed the last-minute move by the outgoing administration in his confirmation hearings.

“I, too, was surprised to see something of this nature done on the way out the door. Certainly, if confirmed, I’m going to work with the FHA administrator and other experts to really examine that policy,” Carson said in response to a question from Sen. Patrick Toomey, R-Pa.

FHA delinquencies are still relatively low overall, and the cause of the spike is impossible to know for sure without more data. It could be an outlier, or it could be the result of lenders lowering FICO credit scores for recent borrowers. While FHA’s minimum credit score is 580, lenders put their own overlays, or safeguards, on loans following the epic housing crash fueled by subprime lending. Average credit scores for new FHA loans were around 700 in 2010-2011. They have since fallen to around 675 in 2016.

“As we’ve seen the economy improve and home values rise and workforce job numbers continue to improve, some lenders have been more comfortable taking off some of those overlays, not going down to the lows that FHA allows, but it has brought credit scores down,” said Stevens, who supported the Trump administration’s freeze on the mortgage insurance premium cut. “FHA had just gotten back in the black, and we were concerned about unforeseen circumstances that could occur, so it doesn’t surprise me that the Trump administration decided to act and at least slow down any look at reductions in [mortgage insurance premiums] until they really understand the portfolio.”

The FHA insures loans and does not lend money. It requires just 3.5 percent for down payment, plus an upfront and annual premium. During the housing crash, it was the only low-down-payment loan available and is credited with saving overall home sales and assisting struggling borrowers to refinance into lower monthly payments. That, however, came at a price. The FHA’s insurance reserves fell below the statutory mandate in 2013 and needed a $1.7 billion infusion from the U.S. Treasury.

With the reserves recovered and the FHA on far stronger footing, outgoing HUD Secretary Julian Castro announced the premium cut on Jan. 9, claiming the FHA could handle any additional risk.

“After four straight years of growth and with sufficient reserves on hand to meet future claims, it’s time for FHA to pass along some modest savings to working families,” Castro said. “This is a fiscally responsible measure to price our mortgage insurance in a way that protects our insurance fund while preserving the dream of homeownership for credit-qualified borrowers.”

There were, however, signs as recently as last fall that FHA loans were beginning to fail at a higher rate. In October, ATTOM Data Solutions, a foreclosure sales and analytics company, reported the biggest jump in foreclosure activity since 2007, with FHA loans behind the surge.

“While some states are still slogging through the remnants of the last housing crisis, the foreclosure activity increases in states such as Arizona, Colorado and Georgia are more heavily tied to loans originated since 2009 — after most of the risky lending fueling the last housing boom had stopped,” said Daren Blomquist, senior vice president at Attom Data Solutions.