With real estate being so competitive, may investors are

investigating real estate mortgages.

This short video explains the variables.. WATCH HERE

Real Estate Note Buyers and Seller Carry Consultants

With real estate being so competitive, may investors are

investigating real estate mortgages.

This short video explains the variables.. WATCH HERE

Pending home sales rose in December for the third straight month, providing further evidence that 2017 was a positive year for housing, but the National Association of Realtors doesn’t expect the good times to keep rolling.

was a positive year for housing, but the National Association of Realtors doesn’t expect the good times to keep rolling.

Recent data from NAR, the Census Bureau and the Department of Housing and Urban Development showed that 2017 was the best year for new home sales and existing home sales in a decade.

Now, new data from NAR shows that pending home sales rose in December to the highest level since March 2017, but NAR is concerned that Republican-led tax reform will dent home sales in 2018.

According to a new report from NAR, which was released Wednesday, the Pending Home Sales Index, a forward-looking indicator based on contract signings, increased 0.5% to 110.1 in December from an upwardly revised 109.6 in November.

That marks the third straight month that the index has increased.

But combine continually low housing inventory and the Republican tax plan, which President Donald Trump signed into law late last year, and you have a recipe for a slowdown, according to NAR Chief Economist Lawrence Yun.

“Another month of modest increases in contract activity is evidence that the housing market has a small trace of momentum at the start of 2018. Jobs are plentiful, wages are finally climbing and the prospect of higher mortgage rates are perhaps encouraging more aspiring buyers to begin their search now,” Yun said.

“Sadly, these positive indicators may not lead to a stronger sales pace,” Yun added. “Buyers throughout the country continue to be hamstrung by record low supply levels that are pushing up prices – especially at the lower end of the market.”

According to NAR, there’s an “imbalance” of supply and demand, which has led to price increases of 5% or more for each of the last six years, but Yun expects that to slow this year.

Yun said that while tight inventories are still expected to put upward pressure on prices in most areas this year, he expects overall price growth to shrink, with some states even experiencing a decline, due to the negative effect the changes to the mortgage interest deduction and state and local deductions under the new tax law.

“In the short term, the larger paychecks most households will see from the tax cuts may give prospective buyers the ability to save for a larger down payment this year, and the healthy labor economy and job market will continue to boost demand,” Yun said. “However, there’s no doubt the nation’s most expensive markets with high property taxes are going to be adversely impacted by the tax law.”

Three of the states where the tax bill’s changes to property tax deductions are expected to have a significant impact are already threatening to sue the government over the tax bill.

Last week, the governors of New York, New Jersey, and Connecticut said they plan to sue the government due to the Tax Cuts and Jobs Act’s elimination of certain state and local tax deductions.

The tax bill installs a cap of $10,000 on state and local tax deductions, but several states (including New York, New Jersey, and Connecticut) have state and local tax burdens that far exceed $10,000.

Yun said that he anticipates the changes to the SALT deduction rules to disproportionally impact certain segments of the housing market.

“Just how severe is still uncertain, but with homeownership now less incentivized in the tax code, sellers in the upper end of the market may have to adjust their price expectations if they want to trade down or move to less expensive areas,” Yun said. “This could in turn lead to both a decrease in sales and home values.”

Topic

INVESTMENT GOALS & EXPECTATIONS

Our February Note Investors Forum Meeting will followup

on Stan Harley’s presentation– Taking what he shared and incorporating that with with YOUR individual goals. What is most important to you? Cash Flow or Capital Accumulation.

Or……………And more specifically how does risk tolerance fit into your needs and expectations.

We’ll consider Performing and Non-Performing notes

How note due diligence can expand your expectations.

Case studies with 2 special out of state note investors

Click Here for more information

February 6th

Dobson Ranch Inn Fiesta Bar & Grill

1644 S. Dobson Rd

Mesa, AZ

SW Corner of Dobson & RT 60 – Superstition Freeway

Every month Capstone Capital USA, LLC hosts the Phoenix Note Investors Forum. Yesterday January 4, we had the pleasure of having Stan Harley if the Harley Mark![]() et Letter share his Technical Analysis of the Financial Markets. More specifically —TRENDS and CYCLES in REAL ESTATE, INTEREST RATES, and the STOCK MARKET.

et Letter share his Technical Analysis of the Financial Markets. More specifically —TRENDS and CYCLES in REAL ESTATE, INTEREST RATES, and the STOCK MARKET.

There were over 65 luncheon attendees who had the unique opportunity to view the financial  markets from a true market analyst.

markets from a true market analyst.

Bottom line–per Stan, the economy will be fine until 2022 or, then we could be in for some challenging times. The full report can be found here:

Cycles in Home Prices Interest Rates and the Stock Market – Phoenix Area Note Investors  Forum – Stan Harley – January 04 2018

Forum – Stan Harley – January 04 2018

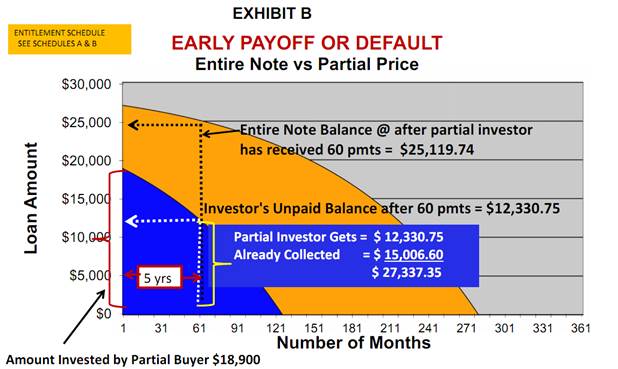

Today an IRA administrator questioned -requested an explanation on the sale of a partial. He said he had never seen this type of transaction before. Neither had his compliance officer.

They were confused and requested a simple explanation which follows.

All of the following statements are true:

“Bob” is buying 3 partials–funding the last purchase of 125 payments(blue) for $18,900.

My entity is keeping the remaining payments –gold(the tail).My entity is assigning all the payments to him as evidenced by an allonge which keeps this transaction SEC compliant.

This is a great deal for Bob, because I will always be in the deal protecting the remaining payments(gold).

After Bob receives his payments, the remaining payments will be reconveyed to my entity as evidenced by a Reconveyance of Agreement for Deed which references the Purchase and Sale Agreement.

In the event of an early payoff, default or if Bob opts to exercise the 60 month buy back provision the following chart –the Entitlement Schedule –Schedule B illustrates how that scenario will be administered.

![]()

The IRA Administrator has executed the following docs:

Bob will record the Assignment of Contract for Deed to protect himself and will have the original note and the allonge(transfers the note) which will be archived by the Servicier and distribute the 125 payments to Bob. In the event of an early payoff or if the purchaser wants to exercise his 60 month option for an early buyback, his administrator as a road map for future reference.

The IRA company rep understood this transaction when explained in plain English. Additionally he received the following Partial from our NoteHolder’s Handbook–Note Holders Handbook_Partials.

A partial is one of the safest ways to invest in notes.

The IRA Administrator thanked me for providing a “Great explanation!”

Proper and detailed due diligence is a must in purchasing a quality note. The note overview provided for each note in the note vault is a summary of what our underwriting has determined to be important points to consider when purchasing note. Let’s look at them line by line.

Proper and detailed due diligence is a must in purchasing a quality note. The note overview provided for each note in the note vault is a summary of what our underwriting has determined to be important points to consider when purchasing note. Let’s look at them line by line.

TYPE–means the type of security. It could be a land contract, mortgage or deed of trust

CFD — means Land Contract, Contract for Deed or Agreement for Deed all of which are synonymous.

VALUE–is the value we have determined usually by a BPO(broker price opinion), sometimes referred to as a CMA(Competitive Market Analysis)

CURRENT BALANCE–is the current loan balance some times referred to as UPB–unpaid principle balance

ORIGINAL BALANCE–is the original when the loan was originated

P & I–meant the amount of the monthly principle and interest payment

ORIGINAL TERM–reflects the # of months of amortization when the loan was originated.

REMAINING TERM–reflects the # of remaining months of amortization.

PAYMENTS FOR SALE–reflects if we are selling all of the note or a piece of the note, meaning a Partial which is further described in this article and in paragraph 4 HERE.

INVESTMENT TO VALUE–reflects the amount of money invested divided by the property value or BPO amount. We consider a good range to not exceed 65%.

LOAN TO VALUE–reflects the amount of the existing loan balance(UPB) divided by the property value or BPO amount. We feel the lower the better, definitely less than 60-65%. The lower the better. The lower the better the equity position in the event something goes wrong with the payments.

INTEREST RATE-is the amount of interest the payor(borrower) is paying.

EFFECTIVE YIELD-is what is your rate of return based upon how much one is paying for the loan compared to the actual remaining loan balance.

SEASONING-reflects how many months the borrower has been paying since the loan was originated.

PAYMENT HISTORY-is a record–a spreadsheet of the payments which include due date, paid date, late fees, taxes and insurance payments and multiple other items. As long as the borrower is current 11 out of 12 months, it is considered to be a good history. As long as the borrower pays within 30 days of the due date even though there may be a late fee charged, we consider that to be on time payments.

ACH-means the payments are automatic bank drafts from the borrowers account. As lenders we really like that typo of borrower.

PAYOR—another word for borrower

DODD-FRANK FRIENDLY–refers to the Dodd-Frank Act which was effective January 10, 2014. Any loans originated after that date require underwriting by a loan originator.

PROJECTED RENT–reflects what that typo home rents for in the area. We use that as a benchmark for the payor–meaning we like to see their total payments to be less than a typical area rental. They have to live somewhere. If rents in the area are much more than their monthly PITI, it is less likely the payor will default.

For additional information on due diligence go to this posting.

Go to our NOTE VAULT for our current performing note inventory.

By Jessica Edgerton, NAR associate counsel

By Jessica Edgerton, NAR associate counsel

In recent months, real estate professionals have reported an upswing in a particularly insidious wire scam. A hacker will break into a licensee’s e-mail account to obtain information about upcoming real estate transactions. After monitoring the account to determine the likely timing of a close, the hacker will send an e-mail to the buyer, posing either as the title company representative or as the licensee. The fraudulent e-mail will contain new wiring instructions or routing information, and will request that the buyer send transaction-related funds accordingly. Unfortunately, some buyers have fallen for this scheme, and have lost money.

A possible red flag to be aware of, and to alert clients to, is any reference to a “SWIFT wire” transaction, a term that indicates an overseas destination for the funds. However, unlike many other e-mail-based “phishing” schemes, this particular manifestation appears to be more sophisticated and less recognizable as fraud. The communications do not contain the typical grammatical or stylistic oddities that are often present in scam e-mails. In addition, because the perpetrator has been monitoring the licensee’s e-mail account, the fraudulent communication may include detailed and accurate information pertaining to the real estate transaction, including existing wire and banking information, file numbers, and key dates, names, and addresses. Finally, the e-mails may come from what appears to be a legitimate e-mail address, either because the thief has successfully created a sham account containing a legitimate business’s name, or because he or she is sending the e-mail from a truly legitimate—albeit hacked––account.

Be aware, also, that this particular scheme is only one of many forms of online fraud being perpetrated against real estate licensees and their clients. In protecting all parties to a real estate transaction from cybercrime, real estate professionals should consider the following guidance:

1. Prevention.

The best line of defense against fraudsters is to make sure that all parties involved in a real estate transaction implement security measures before a cyberattack occurs. These measures include the following:

2. Damage Control.

If you believe your e-mail or any other account has been hacked, you should take the following steps:

This advice is not all-inclusive, and real estate practitioners should work with Information Technology and cybersecurity professionals to ensure that their e-mail accounts, online systems, and business practices are as secure and up-to-date as possible.

This article was also published by the Arizona Association of Realtors.

It is not unusual for a note holed to sell their note to get a certain amount of cash. But………….when given a quote by a note buyer many time they are shocked at the huge discount and insulted—maybe even angry that a note broker or buyer would try to “steal” their “good” paying note. Any proficient note buyer / broker will offer alternatives in the form of quoting to buy a piece or just some of the outstanding balance. Have you ever bought a full pizza? Have you ever bought just a few pieces of piz za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

za? They can sell a whole pizza or sell it by the slice or several slices. Same principle. As the note owner you are selling some of the payments vs all the payments. By doing so your discount is less and you still have the back end principle / payments or “tail” reverting back to you when the partial note buyer receives all of their purchased payments. The majority of these note sellers are not aware of or familiar with partials.

Sometimes as a note owner you only need a specific amount of cash. Selling the whole note makes no cents. There are multiple ways to architect a partial sale. You can sell 12, 24, 60,100 or however many of payments to bring you the cash your need. For the next x# of months, those payments would go to the partial note buyer. After the buyer is paid back, the remaining payments would revert back to you.

Selling a partial gives the note seller a great amount of flexibility. Partials are always a great tool to use when the note holder has an immediate cash requirement and only needs a specific amount of money to cover a specific situation or for a specific purpose. A partial minimizes the discount and frees up cash. It is the best of the best. The terms of the note remain the same for the note payor/borrower. The only thing that changes is the payments are directed to the third party servicing company. Additionally there is contractual language giving the partial buyer the right of first refusal to buy additional payments if they so choose.

What about an early payoff?

Many notes do pay off early. The average time a house or note is paid off historically is 7 – 10 years. If it is paid off early, there are contractual agreements / documents from the outset that are managed by the third party note servicing company determining the payoff and or re-conveyance.

What if the note goes into default?

Unfortunately some notes/mortgages do go into default. IT is a realty of the financial world. If in fact that happens, the contractual agreement spells out the options. Either a buy back from the partial buyer or proceed with the foreclosure /eviction process with the goal of taking back the property and resell it for fair market value. Both the original note buyer and the partial buyer benefit. The partial buyer is made whole with the balance going to the original note seller.

Three Real Life Case Studies

Houston, TX 11/30/15 – Single Family house

Gerry owned a note on a single family house in a so-so area of Houston. He needed money for some personal issues and needed help. I offered to buy the full at a larger discount due to the issues noted below. He was not real enthused with the offer, so we agreed to a partial purchase.

Deal Points

Good Points

Gerry negotiated a great terms with a sort-of strong buyer. Meaning the buyer put down a very strong $14,000 on a $60,000 purchase resulting in a great Loan to Value(LTV). The 7% interest rate was OK. It had a relatively short amortization period of 60 months with a great on time pay history. The 3 Buyer’s FICO scores were weak, but they had a good job history.

Marginal Points

Due to the drop in oil, Houston lost 44,000 jobs. The neighborhood had some marginal houses, but in the process of changing for the good. For these two items, if felt uncomfortable with a full purchase.

Bottom Line

We bought a 24 month partial with the option to purchase the balance in 15 months. It was a secure, safe purchase and Gerry received what he needed. Out Investment to Value was a very secure 26% with a safe Loan to Value of 57%. The graph depicts what we purchased(blue) and what the seller kept. Within one year we bought the gold portion all in our IRA.

Fast forward 11/30/16

Gerry called requesting if Capstone would be interested in purchasing the balance of his note. He had a lingering debt situation. After a short due diligence period, we closed within 10 days. Again Gerry was happy and we were happy owning the full note. Three weeks later we sold the full note to one of our Note Investor Forum Meetup attendees for his ROTH IRA.

Summary

The note seller had a situation, we provided him a solution—twice. The Meetup attendee was in his early 70’s. He wanted a higher yielding note with a shorter amortization period. This was his first note purchase. He is excited to buy additional opportunities.

_____________________________________________________________

Salem, OR 12/20/16 – Land Parcel

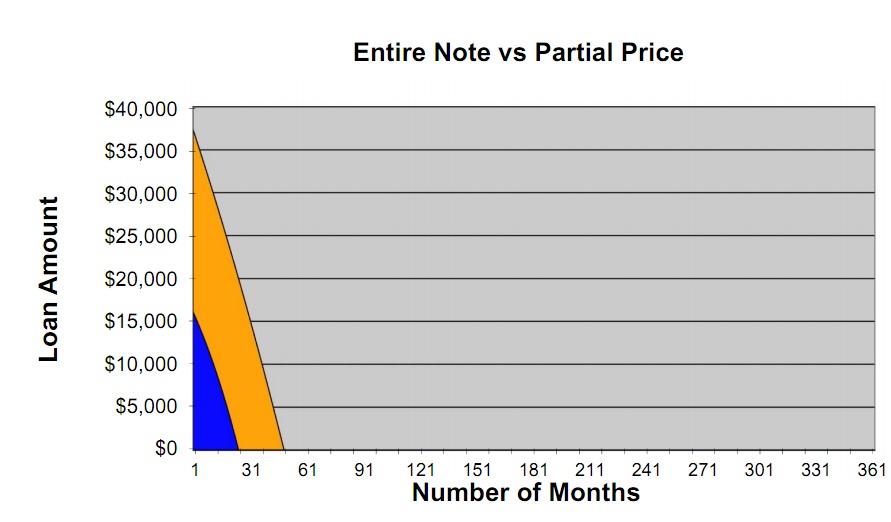

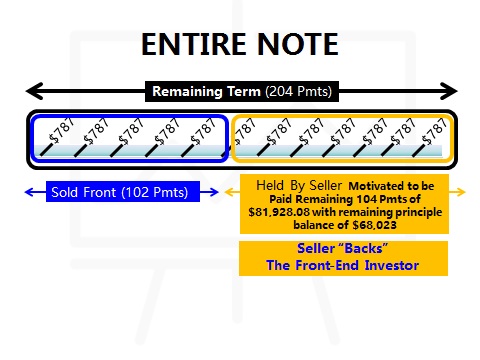

A note colleague referred his friend Kirt his client, Joyce who owned a 13.17  acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

acre out parcel. This was the remainder of a larger parcel where she sold other acreage for a large apartment complex. Joyce wanted funding to purchase some precious metals and have money for a small down payment on a new house. We presented two options—a full purchase and a 102 month partial. She accepted the partial due to the smaller discount and liked the idea of the remaining balance of $68,023 coming back to her in 102 months.

Deal Points

Good Points

Joyce’s buyer had a very good job as a helicopter pilot earning close to $150,000/yr. The servicing company provided a very stable 36 month payment history. She also had a survey of the land which had all utilities. Most likely in the future the apartment complex would expand—buying out the pilot and our partial.

Marginal Points

Joyce did not negotiate good note terms. Only a 4% interest rate (her realtor said that was fair). In reality for land it should have been at least 10%.

Bottom Line

We bought a 102 month partial with the option to purchase the balance in the future. It was a secure, safe purchase and Joyce received the funds she needed. We had a very strong ITV of 11% . It was a true win-win. Our referral partner received a referral fee and sold some gold to Joyce. Joyce was able to buy her house and the Capstone investor had a very safe and secure partial note investment in her mothers’ IRA.

Fast forward 4/5/17

Joyce called stating that she wanted to sell the remaining 102 payments ($68,023) which we did for $19,377. She did not want to wait 102 months to cash out the remaining payments. Joyce got what she needed and we received a fair deal. On the entire transaction, our Investment To Value (ITV) was a very safe 17%, in a fast appreciating real estate market. The odds are high the parcel will be sold for development in the near future providing the investor a very nice return because she bought the note at a steep, but fair discount due to the 4% note rate.

Summary

What really happened though is even more normal. Joyce calls back wanting sell the rest of the back-side far before the re-assignment period. Many not sellers buy into a partial transaction because the transaction mitigates the discount. But…………..more often than not, they will want to sell the remaining balance early to meet life needs.

Partials are a unique method of meeting many needs for note buyers and sellers. They should not be over looked. It is an incredible passive investment vehicle for your ROTH IRA

This Case study was/will be presented at the Note Investors Summit April 5-7, 2018 in Irvine, CA

Investing in real estate notes with yo ur IRA is one of the most popular self-directed IRA investments available. But with this popularity comes common mistakes when people lend their IRA (and non-IRA) money out, secured by liens on real estate. Follow these 10 tips to avoid potentially costly mistakes when choosing real estate as an IRA self-directed investment.

ur IRA is one of the most popular self-directed IRA investments available. But with this popularity comes common mistakes when people lend their IRA (and non-IRA) money out, secured by liens on real estate. Follow these 10 tips to avoid potentially costly mistakes when choosing real estate as an IRA self-directed investment.

1) You may end up owning this piece of real estate if your borrower defaults. Never loan on something you wouldn’t want your IRA to own. The risk of loaning your IRA investments toward real estate notes is matched by the reward: I routinely see yields from these loans at 12% and higher; however, borrowers can default and you may be left with the property in foreclosure. If you would be upset by the potential of taking over this property in foreclosure, you probably should not make the loan.

2) Do not advance IRA money for home repairs until the repairs are finished; then have the repairs inspected before advancing the money. This is one of the biggest mistakes that I see clients make with their IRAs. They fund the full loan amount expecting that the repairs will be done on the property, but the borrower will actually need a little more money on another. If the loan goes bad, the IRA could end up with a property that hasn’t had the necessary repairs.

3) Do not loan money to someone you would feel uncomfortable foreclosing on. William Shakespeare wrote in Hamlet, “Neither a borrower nor a lender be/ For loan oft loses both itself and friend/ And borrowing dulls the edge of husbandry.” For the most part, I cannot agree with this advice, because lending and borrowing money drives our economy and increases economic activity. However, the part about a loan losing a friend is absolutely correct, in my opinion. If foreclosing on your borrower would cause you heartache, it is better not to make the loan. I have seen friendships destroyed over a loan gone bad.

4) If the loan goes into default, take action immediately. No one wants to admit that he or she has made a mistake in self-directed investing, but delaying action can be costly. You can always stop the foreclosure process once it has begun, but you cannot complete the process unless you start it.

5) Collect interest monthly so you will know if the borrower is getting into trouble. Many borrowers, especially investors, would prefer to pay interest at the end of the loan. But this exposes the lender to additional risk. The purpose of collecting payments monthly is both to:

Keep in mind that unless you have contracted for monthly payments, you may not be able to foreclose, even if you do discover that the borrower is in financial trouble, because the loan may not be in default. This has actually happened to some of my clients.

6) If you are unsure about how to evaluate the loan, hire a professional to help you. Although a hallmark of the self-directed IRA is that it is “self-directed” — meaning that you make your own decisions and find your own investments — most IRA owners either do not possess sufficient knowledge or, in my case, sufficient time, to properly evaluate a loan transaction. My solution is to hire a professional to help me with the deals. He checks out the borrower, coordinates with the title company, orders the appraisal and usually a survey, makes sure insurance is in place and generally evaluates the loan. Naturally, he charges a fee for this service, which is passed through to the borrower on top of any interest and fees that my retirement plan may charge. This increases the cost of the loan; but in this case, the non-Biblical version of the golden rule applies, which is “He who has the gold makes the rules.”

7) Get title insurance for the loan. The purpose of title insurance is to shift risk away from you and to the title company. In Texas, where my office is, the incremental cost of title insurance is very small when issued in conjunction with an owner’s title policy. Regardless of the cost, making sure that your IRA is protected from title flaws is important.

8) Verify that hazard and, if necessary, flood insurance is in place, naming your IRA as an additional insured. It is very easy to miss this issue when you are trying to get everything completed right before a closing. Borrowers may get insurance at the last moment and simply forget to add your IRA as an insured. But if something goes wrong, you will want to make sure your IRA is named on the check.

9) Insist that the borrower provides you with evidence of payment when property taxes and homeowners association fees become due. The same thing would apply to hazard and flood insurance premiums, although normally you would receive notice of cancellation for non-payment of those bills. Depending on where you live, property tax bills can increase quickly due to penalties and court costs, which reduces your equity position in the property.

10) Get a personal guarantee if lending to an entity or to an individual with some weakness. When things are going well, you might be tempted not to insist on a personal guarantee, and indeed many borrowers will resist this. However, as we all have discovered recently, circumstances do change, and a personal guarantee may be helpful in collecting the debt. I collected on a note once where the property had decreased substantially in value due to vandalism and market conditions. Instead of foreclosing, I had my lawyer send a letter explaining to the guarantor, who had a significant amount of assets, that he was personally liable on the debt and that if he were unable to satisfy the note, I would pursue legal action against him and the borrower. A week later, a cashier’s check showed up that satisfied the lien.

There’s more to know when considering real estate for your self-directed IRA

This list of suggestions is not meant to be exhaustive. Other issues you will need to understand include:

Always get good legal counsel to assist you with loan documentation. Because the borrower traditionally pays for all expenses including legal fees, there is no reason not to have an attorney draw up loan documents.

Lending can be an excellent investment in an IRA. It is relatively easy to do and, if done correctly, has a comparatively low risk. Getting to know successful real estate entrepreneurs who borrow your IRA money may also lead to other, intangible benefits as well. Finally, be sure to learn the pointers for buying real estate with your self-directed IRA before you take any actions.

H. Quincy Long is a certified IRA services professional (CISP) and an attorney and is the president of Quest IRA, Inc., with offices in Houston and Dallas, Texas, as well as, Mason, Michigan. Email him atQuincy@QuestIRA.com.

Nothing in this article is intended as tax, legal or investment advice.

The housing recovery that began in 2012 has lifted the overall market but left behind a broad swath of the middle class, threatening to create a generation of permanent renters and sowing economic anxiety and frustration for millions of Americans.

Home prices rose in 83% of the nation’s 178 major real-estate markets in the second quarter, according to figures released Wednesday by the National Association of Realtors. Overall prices are now just 2% below the peak reached in July 2006, according to S&P CoreLogic Case-Shiller Indices.

But most of the price gains, economists said, stem from a lack of fresh supply rather than a surge of buyers. The pace of new home construction remains at levels typically associated with recessions, while the homeownership rate in the second quarter was at its lowest point since the Census Bureau began tracking quarterly data in 1965 and the share of first-time home purchases remains mired near three-decade lows.

The lopsided recovery has shut out millions of aspiring homeowners who have been forced to rent because of damaged credit, swelling student loans, tough credit standards and a dearth of affordable homes, economists said.

In all, some 200,000 to 300,000 fewer U.S. households are purchasing a new home each year than would during normal market conditions, estimates Ken Rosen, chairman of the Fisher Center of Real Estate and Urban Economics at the University of California at Berkeley.

“I don’t think we are in a normal housing market,” said Lawrence Yun, chief economist at the National Association of Realtors. “The losers are clearly the rising rental population that isn’t able to participate in this housing equity appreciation. They are missing out on [a big] source of middle-class wealth.”

Anxiety about missed economic opportunities is a key driver of the anti-incumbent anger on both sides of the political spectrum that has shaken up the 2016 election season, helping fuel the insurgent presidential campaigns of Donald Trump and Bernie Sanders.

“You have these people who can’t get housing, and it’s turning into this rage,” said Kevin Finkel, executive vice president at Philadelphia-based Resource Real Estate, which owns or manages 25,550 apartments around the U.S.

While economists expected the homeownership rate to begin edging up this year, the rate fell to a 51-year low of 62.9% in the second quarter from 63.4% in the same quarter last year.

The rate could fall to 58% or lower by 2050, according to a recent prediction by housing experts Arthur Acolin of the University of Southern California, Laurie Goodman of the Urban Institute and Susan Wachter of the Wharton School at the University of Pennsylvania.

Long-term declines could erase gains made by middle-class Americans since World War II. Owning a home provides protection against rising rents and has been a key component of retirement saving and wealth creation.

“The default savings mechanism for American households has been homeownership,” Ms. Wachter said. “Today we have historic lows for young households in terms of ownership so they’re not getting on this path.”

That, in turn, can ripple throughout the economy. Homeowners often use home equity to pay for college tuition, vacations or home renovations, all of which help boost consumer spending. The mere knowledge that home values are rising can make consumers comfortable spending money other places, a process known as the wealth effect.

“We’re seeing a divide between the wealth of homeowners and the wealth of renters,” said Nela Richardson, chief economist at real-estate brokerage firm Redfin.

After peaking in July 2006, the Case-Shiller index plunged 27% over the next six years. Since then the recovery has been swift, particularly in markets with strong job growth and limited supply, creating problems for entry-level buyers in particular.

Across the country the recovery has been divided between strong West Coast markets and Texas, which have rebounded swiftly beyond their 2006 peaks, while prices from the Rust Belt to southern Florida may not return to those levels for decades.

Prices in the Boulder, Colo., metro area are 45% above their prior peak, while those in Dallas are 26% above their boom-time highs, according to data provider CoreLogic Inc. Meanwhile, prices in the Saginaw, Mich., area remain nearly 40% below their peak levels and those in Atlantic City are still 38% lower.

In Sacramento, prices have jumped 64% since the beginning of 2012, according to CoreLogic.

Sunny Kenner, a 40-year-old single mother who works for the county government and has rented for years, decided a few months ago she needed to buy before rising prices shut her out for good.

Ms. Kenner, who is looking for a two-bedroom house in the $250,000 range, has been trying for months but twice has been outbid by buyers with large cash reserves who bid $10,000 over the asking price. By the second day a house is on the market, she says, there are usually about half a dozen offers on it.

“The first time I didn’t get one of the houses, of course, I cried,” she said. “The second time I was just numb.” She said she wishes she had enough money to buy when prices hit bottom a few years ago. “I feel like I missed the boat.”

The main reason for falling homeownership, economists say: mortgage availability. Lenders chastened by the financial crisis have been fearful of making loans to borrowers with dings on their credit, student debt or credit-card bills, or younger buyers with shorter credit histories.

“I’m not sure that we’ll see some of those conditions change in any material way in the foreseeable future,” said Tim Mayopoulos, the president and chief executive officer of mortgage giant Fannie Mae, in an interview last week.

“Right now our mortgage finance system is still not working well for lower- and middle-income households and first-time buyers,” added Mr. Rosen.

A dearth of home construction, especially at the lower end, is taking a toll. Nationally, the inventory of homes for sale has dropped more than 37% since 2011, according to Zillow, a real estate information firm. Some of that reflects the clearing away of distressed inventory, but economists said the pendulum has swung toward a housing shortage.

An estimated 1 million new households were formed last year, but only 620,000 new housing units were built, according to the Urban Institute. An analysis of census data by the Urban Institute showed that all of the net new households formed between 2006 and 2014 were renters rather than owners.

In 2006 home builders produced 40% more single-family homes than the 30-year long-run average. Last year, by contrast, single-family home construction was still 30% below that mark, according to Census Bureau data.

“We went so many years without building there are in many places in the country a shortage of housing,” said Richard Green, the Lusk Chair in Real Estate at the University of Southern California. “I think that overshadows everything else in terms of normalcy.”

In the early years of the recovery only top earners could afford to buy homes, as new buyers struggled with joblessness or tarnished credit histories, so builders focused almost exclusively on the high-end.

“The entry-level buyer, up until recently, has not been that involved in buying houses,” said Dale Francescon, co-chief executive of Century Communities, a publicly traded builder that operates in four states. “That’s historically where a significant amount of the volume has come from.”

Even as first-time buyers have started returning to the market, many builders have been slow to respond. Building lower-priced homes means finding cheaper land, and that tends to be farther away from job centers on the suburban fringes.

Those areas were the hardest hit during the housing bust, and many investors have been hesitant to encourage builders to return. As a result, builders have tended to focus on ever-dwindling and increasingly expensive land in core areas, pushing up the prices.

Tom Farrell, director of business development for Landmark Capital Advisors, which counsels investors on real-estate projects, said risk appetite is low, particularly outside core markets.

“We’re often saying ’You all want to be in the same spot, and you’re tripping over each other,” he said. “It’s just difficult to get people out to those secondary markets.”

OUR OPINION

This gives more credence to seller financed notes, thus creating even more of an opportunity.